Twitter reported its earnings this afternoon, and I’ve been sharing some quick thoughts and charts on Twitter itself, appropriately. I’m a massive Twitter fan and user, and it’s enormously important to my business, but I continue to be somewhat bearish on its potential as a business, as my earlier posts will show. This quarter’s results did little to change that perception.

MAU growth better but not great

There are lots of ways to look at Twitter’s monthly active user numbers, but they all show more or less the same picture:

The fact is that, no matter how you look at it, there’s progress here, but it’s minimal. A year after taking over at CEO, Jack Dorsey still has precious little to show as far as returning his beloved Twitter to user growth, and that should be unacceptable to investors. Long-term, Twitter has to outgrow its present size and scope, and the company isn’t doing enough to make that happen. This older post outlines my thinking about how best to do this.

The fact is that, no matter how you look at it, there’s progress here, but it’s minimal. A year after taking over at CEO, Jack Dorsey still has precious little to show as far as returning his beloved Twitter to user growth, and that should be unacceptable to investors. Long-term, Twitter has to outgrow its present size and scope, and the company isn’t doing enough to make that happen. This older post outlines my thinking about how best to do this.

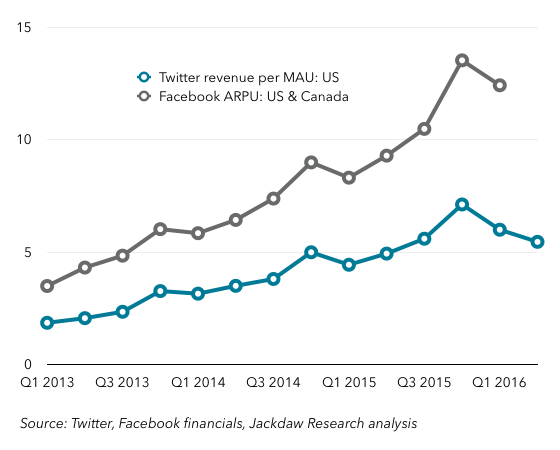

Worrying trends in US ARPU

The other worrying thing is that US ARPU seems to have dropped instead of rising last quarter, which shouldn’t be happening given overall trends and past patterns – I’ve included Facebook’s ARPU up to Q1 2016 as a comparison: As you can see, both companies typically see a spike in Q4 each year – something that every ad company sees – followed by a drop in Q1, but then a return to growth in Q2. Twitter has seen that pattern in the past, as has Facebook, but not this quarter, when ARPU dropped back to below Q3 2015 levels. I haven’t seen an explanation for that yet, but it’s absolutely not the sort of thing Twitter or its investors should want to see happen right now.

As you can see, both companies typically see a spike in Q4 each year – something that every ad company sees – followed by a drop in Q1, but then a return to growth in Q2. Twitter has seen that pattern in the past, as has Facebook, but not this quarter, when ARPU dropped back to below Q3 2015 levels. I haven’t seen an explanation for that yet, but it’s absolutely not the sort of thing Twitter or its investors should want to see happen right now.

There is some interesting commentary in Twitter’s shareholder letter about its ad rates and how they’re positioned in the market. Though there’s careful and somewhat wishy washy language in there, the biggest challenge is that CPMs are too high, and Twitter isn’t doing enough to justify its price premium. It sounds like it will now work on that, but again it feels like we’re seeing a “coming soon” sign where we should have seen real progress by now. This has been a known issue for months, and yet Twitter hasn’t done enough about it.

Live video and monetization

Lastly, live video, which seems to be Twitter’s big focus from a user perspective. We’ve already seen some trials of the capability recently, and although the concept is good, the UI needs work. But the bigger issue is that, while everyone else investing in live video is doing it for the ability to sell masses of ads users will actually be forced to watch, in most cases Twitter is investing in non-exclusive video where the vast majority of the ad space is sold by others. Can is make enough money from this marginal opportunity to make it worthwhile? Will it be a meaningful contributor to revenue and profits over time? That’s the big question here, and I still don’t feel like we have an answer for it. Meanwhile, the core product experience of Twitter continues to suffer both for existing power users and for the kind of new users Twitter needs to attract. Not good enough, in my opinion.