As part of my media comment on the Apple event, I talked a little about how Apple has rethought the Watch since its initial introduction two years ago. That thought deserves a deeper dive, and although we did discuss it a little on the Beyond Devices Podcast this week, I wanted to elaborate here. The word that I keep using in talking about what has changed is that Apple has refocused the Apple Watch, and it’s done that in two ways:

- It’s refocused the feature set of the Watch

- It’s refocused the Watch portfolio.

Refocusing the feature set

When it comes to the feature set, Apple famously introduced the Watch with an echo of the original iPhone announcement, with a tripartite identity:

- the most advanced timepiece ever created

- a revolutionary new way to connect with others

- a comprehensive health and fitness companion.

Though the health and fitness companion came last on that list of three, it’s rapidly risen to the top in terms of how Apple talks about the device today. Tim Cook referred to it this week as “the ultimate device for a healthy life.” Meanwhile, the communication aspects (represented in that second bullet point above) have faded into the background, barely mentioned in this week’s keynote.

But the other thing that’s been de-emphasized in the refocusing of the Apple Watch is apps, and that’s because apps just haven’t worked on the Watch. In September 2015, Tim Cook described what I refer to as Apple’s playbook for hardware devices in the iPhone era, with a set of bullet points:

- Powerful Hardware

- Modern OS

- New User Experience

- Developer Tools

- App Store.

It’s clear that, both at its initial unveiling and a year later, Apple saw the Apple Watch as another product that fit this model, under which developer tools and the App Store would be critical to its success. I argued at the time that it would have been impossible for Apple to introduce a new piece of hardware in 2015 which didn’t tap into the App Store model, and yet I’m no longer sure of that view. Apps have largely flopped on the Watch. The reasons are simple – the hardware has been underpowered, and under watchOS 1 in particular apps were too dependent on the phone. But even in watchOS 2, Watch apps were too slow to load, because they didn’t maintain state and didn’t update in the background.

WatchOS 3 is intended to fix at least some of these issues, and the CPU and GPU upgrades in Series 2 of the Watch are aimed to improve app performance too. But Apple still didn’t make apps much of a focus at this week’s event. In other words, even with these potential enhancements to app performance, Apple is still focusing most of its messaging around the Watch on fitness features. I suspect that, instead of saying “this time we really got it right” after versions 1 and 2 fell short, Apple is going to quietly give developers time to figure this out, and then perhaps next time around we’ll see a renewed emphasis on how apps are adding value to the Watch. Pokemon Go and other high-profile apps may well help with this effort, but Apple is trying very hard not to oversell it this time around, and I think that’s smart. This particular form of crying “Wolf!” is running dangerously close to falling on deaf ears at this point.

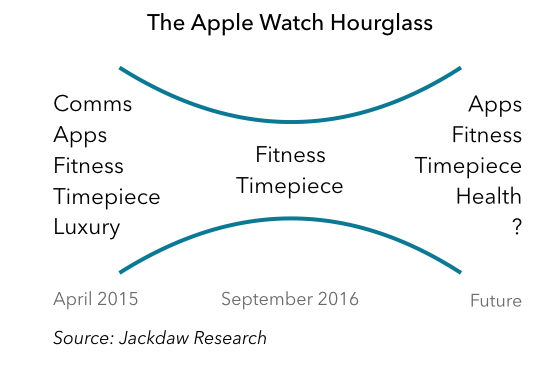

The Apple Watch Hourglass

What I think we may see as a result is a sort of hourglass on its side, as in the diagram below:

The Apple Watch started out trying to be another micro computer. But Apple has now narrowed the focus to mostly being a great timepiece and an increasingly capable fitness device. In time, though, as the apps enhancements kick in and Apple works on other areas like Health in more depth, we may well see the purpose and positioning of the Watch become more expansive again.

The near-term implications of that are important to note: this means the addressable market for the Watch for the time being is mostly about a combination high-end fitness tracker and digital watch, rather than the broader “small computer” market which the iPhone and iPad arguably inhabit, and which is enormously larger. This, in turn, means that the Watch is likely destined for modest, incremental growth over time, rather than the sort of explosive growth that characterized both the iPhone and iPad in their early years. But as Apple begins to think about the Watch more expansively again, so the addressable market will begin to expand, and the sales potential of the Watch will grow with it.

Refocusing the portfolio

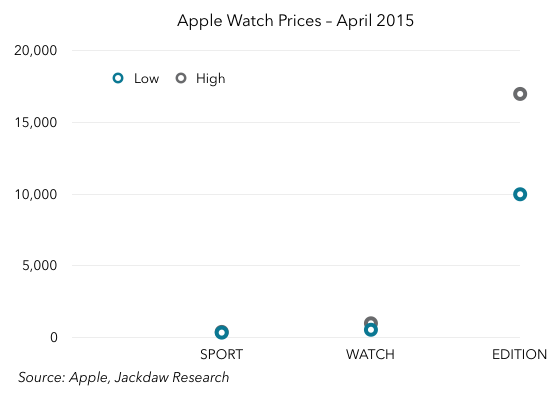

The original Apple Watch portfolio had three distinct tiers, with the Watch the core tier, the Sport the less expensive aluminum version, and the Edition the high-end luxury version, with prices to match. The price ranges for this original portfolio are shown in the chart below:

Two important things to note: the enormous separation between the Sport and Watch versions on the one hand and the Edition on the other, and the sheer height of the Edition portfolio’s pricing, topping out at $17,000. That’s a 48:1 ratio between the most expensive and least expensive Watches.

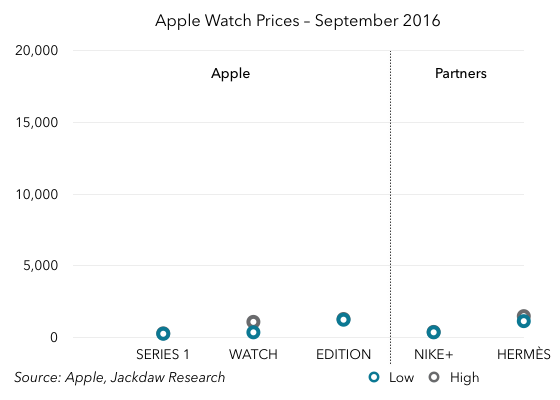

Fast forward a little over a year and you have the new portfolio announced this week, with a slimmed-down Apple portfolio and two partner versions of the Watch as well. For comparability with the chart above, here’s a view of the new pricing to the same scale:

And here’s a version with a scale that makes more sense for today’s Watch pricing (note that the axis tops out at exactly a tenth the price of the axes above):

First things first: Apple has basically eliminated its ultra-luxury Watch Edition models. The only model that has this designation now is the white ceramic Watch, but that’s priced at roughly a tenth of the original Editions. The new price ratio, including the Hermès Watches which actually top out slightly higher than the new Edition watch, is roughly 5.5:1 from most to least expensive. It’s also worth noting that the three Apple ranges are still mutually exclusive but now more or less touch each other — there are no more big gaps in the portfolio, even at the high end. The Series 2 aluminum Watches, starting at $369, pick up just above where the Series 1 Watches leave off at $299, while the Edition hits at $1,249, again just a little above where the Watches peak, at $1,099. The Edition branding still connotes exclusivity and premium materials and therefore satisfy the conspicuous consumption angle, but Apple is now targeting the low end of high-end watches rather than true luxury watches.

Apple now also has its two key Watch partners, Hermès and Nike, to fill in gaps in the portfolio. It’s interesting that we’re seeing these partnerships so early, but I suspect this is another sign that Apple recognizes the nature of this market and its growth prospects. What Apple is doing here is diversifying the portfolio by feature and function early in order to better saturate the smaller addressable market.

Beyond Devices Podcast

If you enjoy these posts, you’ll probably enjoy the Beyond Devices Podcast, in which Aaron Miller and I discuss events like this week’s Apple announcements, as well as other topical issues, and also answer questions about trends in technology.

Our most recent episode is embedded below, and you can find all past episodes on our website, on iTunes, on Overcast, and in other podcasting apps.

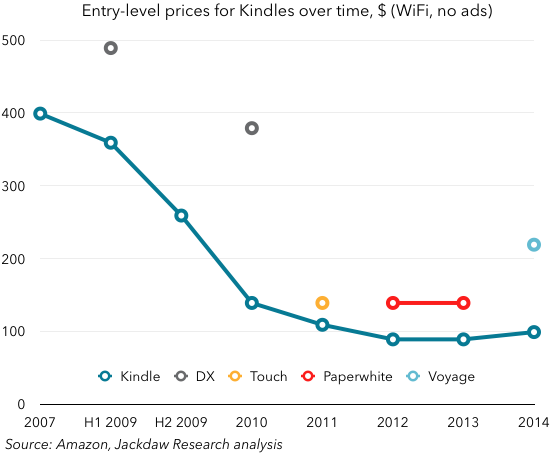

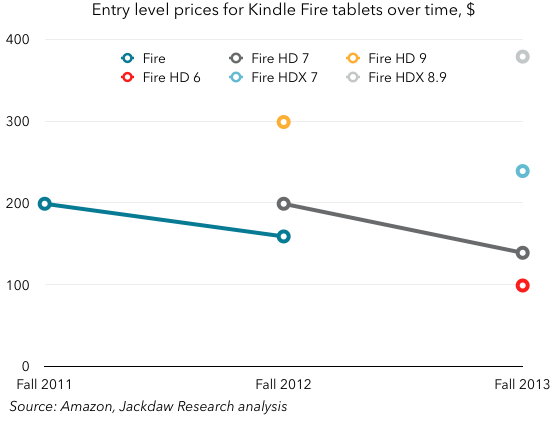

It’s no wonder that there was a slew of articles in late 2011 asking when Kindles would be free, or predicting that they certainly would be shortly (see

It’s no wonder that there was a slew of articles in late 2011 asking when Kindles would be free, or predicting that they certainly would be shortly (see  The trend here is harder to spot, because Amazon hasn’t stuck with a single model throughout the history, rather introducing a series of new models over time. But you can see two distinct trends: individual models have come down in price over time (in the case of the original Fire and the HD 7), while new versions are being introduced at higher prices, actually raising the upper price over time. Amazon has lowered the entry-level price (and you very much get what you pay for at that level) but it’s also moving up the stack into the premium space. The highest base-level price has moved from $200 to $300 to just under $400 over this time.

The trend here is harder to spot, because Amazon hasn’t stuck with a single model throughout the history, rather introducing a series of new models over time. But you can see two distinct trends: individual models have come down in price over time (in the case of the original Fire and the HD 7), while new versions are being introduced at higher prices, actually raising the upper price over time. Amazon has lowered the entry-level price (and you very much get what you pay for at that level) but it’s also moving up the stack into the premium space. The highest base-level price has moved from $200 to $300 to just under $400 over this time.