Note: I’ve added an addendum at the bottom of this post about the content angle specifically.

Verizon buying AOL isn’t a complete surprise – there were rumors of a deal back in January, but now they’ve been confirmed. But it also makes good strategic sense for Verizon as part of a broader strategy that’s been emerging for some time now.

Verizon’s traditional business

Verizon, of course, has its roots in a very different business – landline and wireless telecommunications services. Those make up the vast majority of its revenues today, and its landline business has been going through an interesting transition recently (as I outlined in an earlier post), and in the landline business this means shifting the base from old copper lines to fiber. To be clear, there’s growth left in this business, but it’s highly dependent on the combined value proposition of broadband and pay TV.

A shift in TV viewing requires a hedging strategy

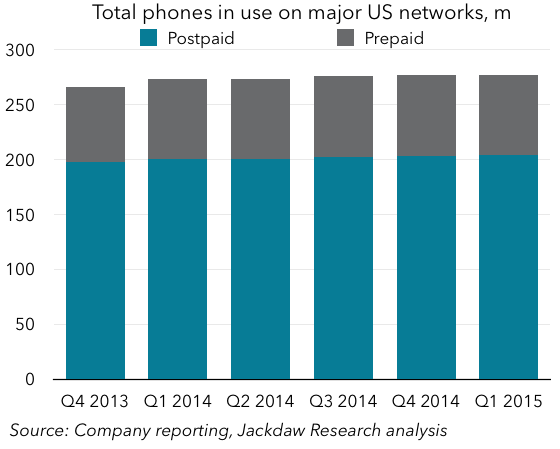

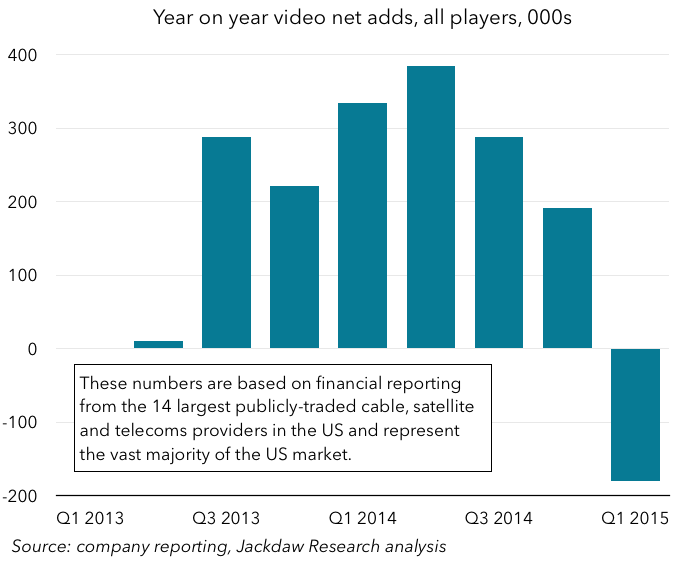

However, the writing is increasingly on the wall for traditional pay TV – disruption is coming, and this quarter marked the first time in recent memory that the major pay TV providers actually saw a decline year on year in TV subscribers:

Verizon recognizes this, and in a previous post I wrote a little about Verizon’s response to this threat to the pay TV business. That response takes the form of a hedging strategy, which allows it to take advantage of the video business even if the traditional pay TV side begins to suffer. I outlined in that post a three-part strategy here (quoting now from that earlier piece):

- Sell classic pay-TV services to as many of the 15 million households where FiOS is available as possible. It’s only sold about a third of those so far, and the number is creeping up pretty slowly, so though there’s growth left, it’s not going to be huge. Competition from cable and satellite remains fierce, so there’s incremental growth here at best. Verizon will continue to evolve the offering here to make more and more content available on more and more screens, but this will be largely a competitive differentiator rather than a source of significant revenue growth.

- Sell a range of wholesale content delivery and related services to third-party content providers like HBO. This is unbounded by the FiOS footprint or even Verizon’s overall broadband footprint, so it could grow significantly from where it is today, though it will always be a much smaller market than consumer video services.

- Sell over-the-top video services to consumers independently of the FiOS offering. This is exemplified by Redbox Instant today, but could well expand into something more. Verizon already has great relationships with all the major content providers through FiOS, and through broader licensing agreements could easily create a sort of unbundled FiOS TV offering to be sold nationwide.

Where AOL fits

AOL fits firmly in the third pillar of this strategy, but also broadens it in several ways:

- It takes the over-the-top content strategy beyond video into news and other forms of content, including Huffington Post, TechCrunch, and so on (it remains to be seen how AOL’s news-focused employees respond to the acquisition, especially given the strong negative reaction to Verizon’s own “news” site a few months back)

- It takes Verizon beyond subscription content and heavily into the advertising sphere, which both provides a more varied set of revenue streams around content but also offers opportunities to provide converged advertising campaigns, retargeting and other attractive elements of a multi-screen advertising platform. It’ll take time to build these linkages, but in time they could be quite powerful for advertisers (see the Cablevision ESPN deal this reported this week).

- It takes these content services beyond the Verizon brand – though Verizon has a national brand, it’s not associated directly with quality content, and though it owns FiOS and therefore a video service, it’s not national. It also doesn’t have a position yet in shorter-form video content. AOL extends it into some of these new areas, and using a different brand that may be more familiar to some potential customers.

The AOL brand

Now, the AOL brand is in some people’s minds forever going to be associated with yesterday’s technologies (my wife’s first reaction to hearing about the deal this morning was “what does AOL do anymore? I just think of “You’ve Got Mail”). But the reality is that AOL remains one of the top online brands in the US in particular, and one of only a handful of companies that reaches over half the US online population with its content each month. AOL, both through its own brand and through powerful sub-brands such as Huffington Post and TechCrunch, is a much more powerful content player than Verizon on a national and especially international basis than Verizon. Yes, there’s some baggage that comes with that, but for the most part the AOL brand family is a great boost for Verizon.

Risks and uncertainties

Despite the strategic sense behind the deal, there are of course risks and uncertainties. There will undoubtedly be a strong culture clash between the two companies – Verizon’s an enormously conservative company in many ways, and although there are pockets of startup mentality, it’s far from the norm across the company. And it’s an absolutely enormous company, much closer in size to AOL Time Warner in its heyday than AOL today. It will be easy for AOL and its culture to be lost or squashed in the course of the acquisition. And although there are lots of synergies (including those described above) on paper, the devil is in the details and it will take a lot of work to identify how these pieces really come together in practice to provide value for the combined company, its customers, its advertisers, and its shareholders. However, on balance I think it’s a good thing that Verizon is willing to take risks as it seeks to navigate uncertain waters in the TV and video space, and this is certainly a much bigger bet than its peer AT&T’s joint venture with Chernin around Otter Media. That, of course, could end up being brilliant or very costly.

Addendum: not just an ad tech play

I’m seeing a lot of people assuming that this deal is entirely about advertising and/or ad tech, and that the content side is either incidental or will be sold off down the line somewhere. However, I’m not as convinced about that, or that the content business at AOL looks the same under Verizon ownership as it did on a standalone basis. Here’s why:

- Verizon is building up to the launch of an over-the-top mobile first subscription video service in the summer. Huffington Post content in particular seems like a great fit in such a service (it may well have been one of the content partners even without an acquisition). With over a hundred million of its own wireless subscribers to market such a service to, Verizon has a great new shopfront for some of the AOL content

- Verizon also provides FiOS within its landline footprint, and some of AOL’s video content could be a great fit there too, as part of traditional bundles, as part of Custom TV (should it survive legal challenges), or in some other form.

- Verizon’s insight into its own users and the 70% of Internet traffic that traverses its network at some point could also allow it to add a very important targeting layer to AOL’s advertising around its own content – the challenge for all online advertisers is how to extend their reach beyond the sites they own – Verizon provides a significant depth of insight about users AOL could never glean itself. This goes the other way too – Verizon can gain insight about users from the time they spend on AOL’s content, even if they can’t monetize that usage directly.

In short, I think AOL’s content businesses have a better shot and a better role under Verizon than they did at AOL, and I’m not convinced they’re just going to be spun off once the merger closes.

As you can see, the number of active users is far smaller than the number of registered users when added to that same chart. In the chart below, I’ve shown PAUs as a percentage of registered users at the four points in time where we have both numbers:

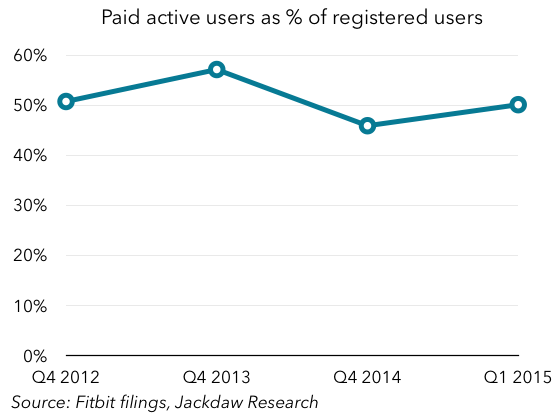

As you can see, the number of active users is far smaller than the number of registered users when added to that same chart. In the chart below, I’ve shown PAUs as a percentage of registered users at the four points in time where we have both numbers: The number bounces around at about 50%, rising or falling a little over time but remaining remarkably constant. In one sense, that’s obviously fairly bad news – in addition to the fact that very few Fitbit buyers purchase a second device, it would appear that half of those who bought one stop using it after a period of time. However, there’s a flip side to this, if you’re looking for a silver lining, which is that the number isn’t falling over time. In other words, over two years ago, the number was 50%, and it still is. I’m actually a bit surprised by this, because all the early abandoners should still show up in the numbers and drag the overall retention rate down, but that doesn’t seem to be happening. What’s interesting is that this correlates closely with a survey I did last year about fitness trackers. The key question here was the individual’s experience with fitness trackers:

The number bounces around at about 50%, rising or falling a little over time but remaining remarkably constant. In one sense, that’s obviously fairly bad news – in addition to the fact that very few Fitbit buyers purchase a second device, it would appear that half of those who bought one stop using it after a period of time. However, there’s a flip side to this, if you’re looking for a silver lining, which is that the number isn’t falling over time. In other words, over two years ago, the number was 50%, and it still is. I’m actually a bit surprised by this, because all the early abandoners should still show up in the numbers and drag the overall retention rate down, but that doesn’t seem to be happening. What’s interesting is that this correlates closely with a survey I did last year about fitness trackers. The key question here was the individual’s experience with fitness trackers: