Note for new readers: this post is part of a series on major tech companies’ earnings for calendar Q3 2014.

I’m going to link here quickly to two of my past posts on Samsung as they provide useful context which I don’t want to revisit in this post:

- Is Samsung’s Exceptionalism Coming to an End? – on Techpinions. This post focused on the fact that Samsung had always seemed an exception to my rules for success in tech, and it seemed inevitable that its reign would sometime come to an end.

- Thoughts on Samsung’s Q2 2014 earnings (and its future) – on this blog. In this post I talked about Samsung’s margins as being unusual for a pure consumer electronics business, and how those margins were likely to revert to the mean eventually because of Samsung’s lack of differentiation. (This is also the most-read of any post on this site since its inception a year ago)

All past analysis on Samsung on this blog can be seen here. My analysis tends to focus on Samsung’s mobile business specifically – other than a brief mention of chips, I won’t cover Samsung Electronics’ other businesses (air conditioning, TVs, refrigerators and display panels, among other things).

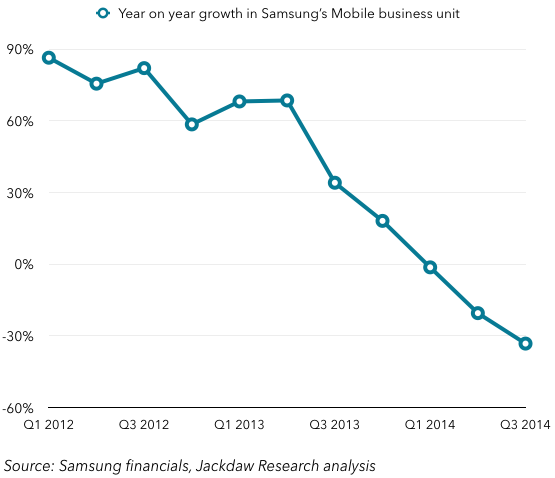

Plunging growth numbers

It’s worth starting with a quick financial review, to make sure we’re all on the same page. The relevant business unit from a mobile point of view is “IM”, or IT and Mobile communications. This includes PCs and tablets as well as smartphones, but it’s the lowest-level division where Samsung reports both revenues and profits, so it’s the one we’ll focus on here. However, it does report revenues for the Mobile segment specifically, so we’ll start there. First, revenue growth:

As you can see, year on year revenue growth has plummeted from positive 90% in Q1 2012 to negative 30% this past quarter. The decline over the past year is alarmingly linear, and one wonders how much worse things can get before that decline levels off.

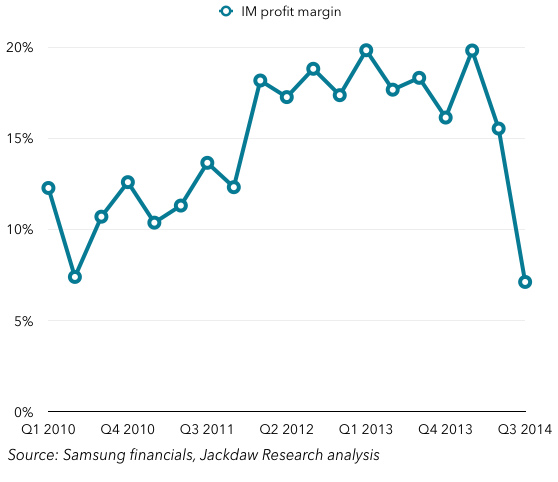

Plummeting operating margins

The major implication of that decline is that margins are getting squeezed:

This margin squeeze is happening for three reasons:

- Scale is critical to margins in the consumer electronics business, and as Samsung’s shipments have fallen from their peak, so their margins have fallen

- Samsung has had to reduce prices to keep shipments up (it says they rose slightly from Q2 to Q3 and major firms such as IDC and Strategy Analytics seem to agree).

- Samsung has enjoyed high share in the premium end of the market, but that is now being challenged, and more of its sales in Q3 came from low-end devices, which are inherently lower margin.

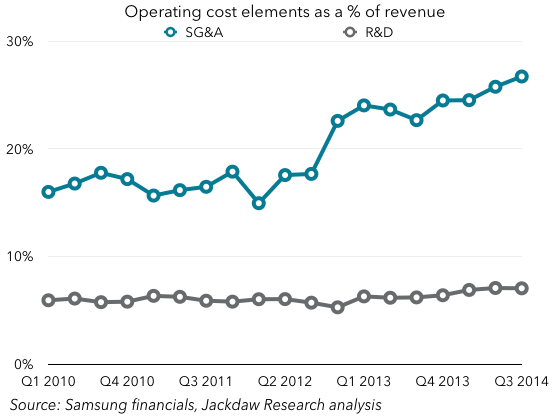

Scaling costs down is much harder than scaling them up

The other big thing that’s afflicting Samsung from a margin perspective, and that’s afflicted other handset businesses which have gone through similar declines in the past, is that it’s much easier to scale costs up with revenue than to scale them down commensurately when revenues start to fall. For example:

- As you’re growing, you grow costs with a time lag to revenue growth. This leads to margin expansion. However, the same time lag on the way down leads to margin contraction, and it’s very hard to keep cost reductions ahead of revenue shrinkage.

- Growth-driven increases in costs reflect success-driven growth, as you hire people because you have a critical need to support that growth. But as you shrink, it’s far less obvious which people are now superfluous. Is this marketing executive or that one the one we don’t need? And can the one we keep reasonably do the job the other was doing in addition to her own?

- Certain costs are clearly tied to volumes, such as manufacturing and distribution, but others are much less clearly so. Once you start cutting, it’s easy to cut in ways that actually undermine growth, and once there’s a company culture of decline, the best people start jumping ship and you’re left with the ones who can’t move on to better things.

Look at Samsung’s two major components of operating costs and see how hard they’re finding it to ramp these down commensurate with the revenue decline, especially the Sales, General and Administrative line:

From Samsung’s best division to an underperformer

The mobile division was for a time Samsung’s best division in a number of ways: easily its largest by revenues, it enjoyed the highest margins for a five-quarter period between 2012 and 2013, and produced the most operating profit from mid 2011 until Q2 of this year. But other than by revenues, it’s now underperforming the chip division in several ways. The semiconductor division has had higher margins for a year, and the gap is now widening significantly:

But the semiconductor division actually generated more operating profit in dollar/Won terms this past quarter. That’s a remarkably rapid shift:

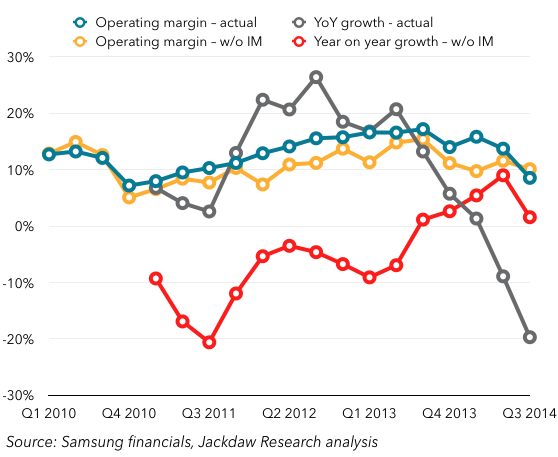

At this point, the mobile division is actually becoming a drag on overall performance, whereas it has previously always raised the overall bar. Focus on the yellow and blue lines in the chart below: the blue line represents actual overall operating margins, which have fallen for the last two quarters, whereas the yellow line represents operating margins for the rest of the business without the IM division. As you can see, the yellow line crossed over the blue line this quarter. Year on year growth for the company as a whole is plummeting too, as the mobile division’s shrinkage drags down the rest of the company, which has actually managed to grow without IM.

The performance of Samsung Electronics overall is shown in the chart below:

Who is Samsung losing to?

I’m seeing Samsung’s decline being variously attributed to Apple and Xiaomi in today’s coverage, but neither of them accounts for the decline in Samsung’s market share. The reality is that Samsung is losing share to a whole variety of other players, and especially to the plethora of low-end, non-name-brand Android players flooding the market. The big six Chinese vendors, Xiaomi among them, doesn’t account for the fall in Samsung’s share, though between them they’re roughly equal in total shipments to Samsung at this point. But it’s really the “All others” line which accounts for Samsung’s decline in share:

And that’s the point here: there isn’t one single thing that’s ailing Samsung. As I’ve written elsewhere, it’s fighting (and losing) on multiple fronts at once:

- Apple continues to gain at the premium end of the market, and the new iPhone 6 and 6 Plus will make the situation even worse there for Samsung

- Other established Android vendors are taking share in the premium segment, especially LG, whose shipments (and margins) continue to rise

- Chinese vendors continue to make significant inroads in China, but Xiaomi is far from the only one, and some of them are making inroads in other emerging markets too, eating into Samsung’s low-end base

- Local vendors in certain other emerging markets, especially India, are also eating into Samsung’s share

- Ultimately, Samsung has failed to differentiate itself as an Android vendor. Nothing it has done for the past few years was inherently difficult for others to copy, especially given time and the emergence of the Shenzhen ecosystem. And that lack of differentiation is coming home to roost now.

Possible solutions

I wrote about this a little last quarter too, so I’ll make this quick:

- New materials: Samsung has talked about this for a while now as a possible cure for its ills. But it misses the point on two fronts: first, if materials were the answer, HTC would be in much better shape than it is; secondly, materials alone are not enough: the kind of people attracted to premium materials are attracted to premium design in general, and both Samsung’s hardware design and its software let it down here. To the extent that there are people who want both Android and good design, they can get it elsewhere and Samsung won’t meet the need just by swapping plastic for metal.

- Chips. I wrote about this last quarter, saying that it was far from clear that Samsung could generate anything like the same revenue and profits from chips as it has from smartphones, even if it repairs its relationship with Apple (itself far from a likely outcome). In addition, much of its success in chips over the past couple of years has likely come from flash and other basic chips, not SoCs, as the author of the AAPLTree blog persuasively argues here. Though Samsung’s chip division is now generating more profits and margins than its mobile division, that’s due entirely to the decline in mobile, not growth in chips.

- Differentiation. Differentiation has always been the key to high margins in consumer electronics, and Samsung has failed to achieve it. Differentiation at the high end would mean a focus not just on premium materials but premium software and services, a far cry from Samsung’s past focus on gimmicks and unattractive UIs. Differentiation at the low end is much tougher, because it comes down to acceptable performance at the lowest price, which others now do at least as well as Samsung. It may have to embrace this strategy regardless, perhaps with a Scion-like sub-brand tailored for this opportunity, but I’m unconvinced that’s the answer.

Overall, I’m pessimistic that Samsung can return to its former performance. I think it’s heading for a new reality, and the biggest question is where the decline stops and at what point Samsung is able to stabilize its business.