Today, Twitter formally introduced its new mobile app install ads product, joining Facebook and Google in what is becoming a crowded space, with Yahoo apparently waiting in the wings too. I had a quick look at this space in the context of Facebook’s Q1 earnings a few weeks ago, but wanted to drill down deeper, especially now that we know more about app revenue through Google Play. The upshot of all of this is that the opportunity for mobile app install advertising, though growing rapidly, is not big enough to provide a significant revenue stream for all these companies. In other words, there’s gold in them there hills, but not enough to justify the gold rush we’re seeing into this space.

First, a quick primer on mobile app economics. Some of the major app companies are public, and report data themselves, while several third parties also report data on the topic regularly, allowing us to draw a few conclusions:

- Revenue from advertising is a factor for some apps, but the vast majority of revenue today (likely between 80% and 90%) comes from pay-per-download and in-app purchases. As such, the revenue numbers for the two major stores – Apple’s App Store and Google Play – likely account for a significant proportion of total revenues from apps 1.

- Developers pay Google, Apple or other stores 30% of their gross revenues from these stores, keeping 70% for themselves. Thus, if they’re to make a living, it will be by keeping their other costs contained within that net revenue figure. That needs to cover development costs, ongoing operating costs (salaries, hosting, care, etc.), and costs to promote apps.

- Sales and marketing costs for most successful app makers sit between 10% and 20% of gross revenues. App install advertising will come out of this budget, and may indeed make up most of it. This percentage may be significantly higher for apps early in their lifecycle and therefore promoting themselves heavily without yet seeing significant revenue, but it will tend to return to that average over time.

- Thus, anywhere between 40% and 50% of a typical app developer’s gross revenue may go to the store commission plus sales and marketing, leaving about half for all the other costs of running the business.

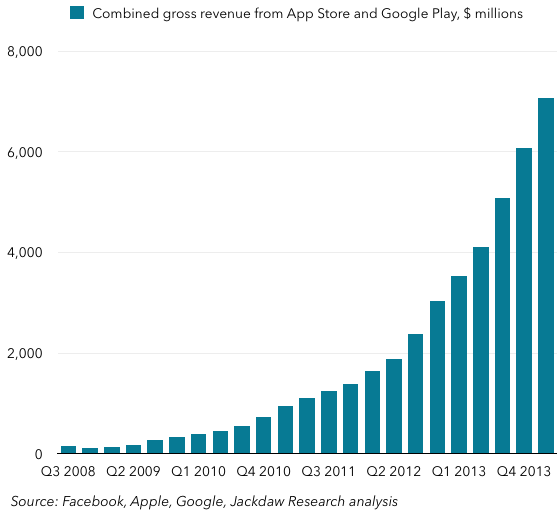

Given these facts, let’s look at total gross revenue opportunity from the two major app stores. I’ve added 15% to my estimated gross revenue from the two stores to account for the advertising opportunity.

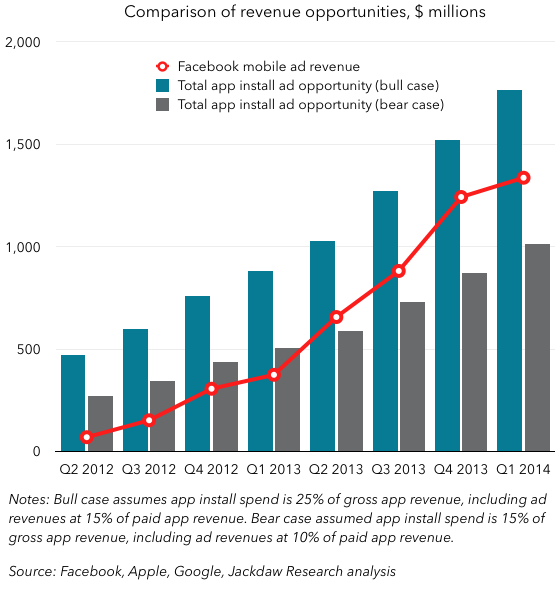

Now, let’s think about the size of the market for mobile app install ads, which as we’ve already said will have to come out of that sales and marketing budget. To put it in context, we’ll compare it to Facebook’s mobile advertising revenues, since Facebook is the largest player in this market today and a substantial proportion of this revenue comes from app-install ads today. In the chart below, I’ve plotted Facebook’s mobile ad revenues against two views of the app install ad opportunity – one a bull case and one a bear case. The bull case assumes that the app install opportunity is 25% of total gross revenues, and adds 15% to store revenues to account for ad revenues. The bear case assumes that the app install opportunity is 15% of gross revenues, and adds a smaller 10% to store revenues to account for ad revenues. My own view is that the bear case is likely closer to reality.

Now, let’s think about the size of the market for mobile app install ads, which as we’ve already said will have to come out of that sales and marketing budget. To put it in context, we’ll compare it to Facebook’s mobile advertising revenues, since Facebook is the largest player in this market today and a substantial proportion of this revenue comes from app-install ads today. In the chart below, I’ve plotted Facebook’s mobile ad revenues against two views of the app install ad opportunity – one a bull case and one a bear case. The bull case assumes that the app install opportunity is 25% of total gross revenues, and adds 15% to store revenues to account for ad revenues. The bear case assumes that the app install opportunity is 15% of gross revenues, and adds a smaller 10% to store revenues to account for ad revenues. My own view is that the bear case is likely closer to reality.

The most obvious message of the chart is that Facebook mobile ad revenue alone is now either very close to the total app install opportunity, or has in fact surpassed it, depending on whether you focus on the bull case or bear case. Either way, the total revenue opportunity today is somewhere between $1 billion and $2 billion per quarter, and growing at a decent clip. But Facebook has had this space largely to itself to date, whereas with Twitter, Google and Yahoo entering, it will have to split this opportunity with these other players.

In the context of total revenues for these four players, this is a small new opportunity. Together, these four companies generated $72 billion in revenue in the four quarters to March 2014, so an additional $4-8 billion is not enormous – amounting to 5-10% or so in additional revenue. If the four companies were to split the opportunity equally, only Twitter would see a more than 25% uplift in revenues.

Much has been said about Facebook’s reliance on app install ads, and I think it’s been overblown. Though it’s clearly benefited from the growth in this category, I think it’s unlikely that these ads make up far more than half of Facebook’s mobile ad revenues in total. But to the extent that this is going to become a much more crowded space with the entry of Twitter, Yahoo and Google, Facebook’s ability to benefit from this opportunity will diminish. As such, it will be very interesting to watch the growth rate in Facebook’s mobile advertising revenues in the next few quarters as it sees increased competition. At the same time, though, these new competitors shouldn’t overestimate the size of the addressable market, which will always be capped at a quarter or less of the total revenue from apps as a matter of basic economics.

Notes:

- For simplicity’s sake, I’m excluding the revenue opportunity through other stores, because they account for a tiny proportion of overall revenues. Adding them in would not significantly affect the numbers. ↩