After a couple of days of talking to various reporters about the Sprint and T-Mobile news from this week, I thought I’d take some time to write up my thoughts on the situation. I already posted some thoughts on Dan Hesse’s tenure at Sprint here. This has turned into a longish post, so here are some signposts for you: the first section deals with why the Sprint-T-Mobile merger made sense, the second deals with where Sprint goes from here, the third deals with where T-Mobile goes from here, and at the end I talk about other issues relating to T-Mobile, namely the other potential merger offers, T-Mobile’s claim to be the largest prepaid carrier in the US, and its goal of catching Sprint by the end of the year (each of those hyperlinks will take you to the relevant part of the post).

Why the merger made sense

I did a long post previously about why the Sprint-T-Mobile merger made sense. If you haven’t read that, I suggest you do, because I won’t cover the same ground in detail again here and the basic arguments haven’t changed even if some of the numbers have. In brief, Sprint and T-Mobile both suffer from their small scale relative to Verizon and AT&T, which manifests itself especially in advertising spend, network costs, retail distribution and purchasing power. Sprint and T-Mobile have attempted to overcome their ad spend disadvantage through various means, Sprint with its Framily plans, which create a viral effect as people try to sign up friends, family and apparently complete strangers; and T-Mobile with its heavy use of social media for marketing. And SoftBank’s acquisition of Sprint and Brightstar has allowed the combined company to generate greater purchasing power in devices and accessories. But a fundamental and significant gap remains.

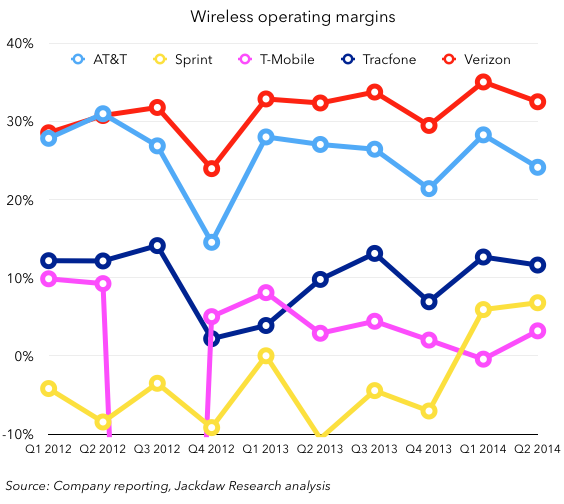

This is evident nowhere so much as in the various companies’ margins, as shown below (this chart is an excerpt from the deep dive on US wireless operators’ Q2 performance which I’ll be publishing early next week. A preview is available on FierceWireless now):

As you can see, both T-Mobile and Sprint are languishing in the single digits, while AT&T and Verizon were at around 25% and over 30% respectively last quarter. This is a direct result of their lack of scale, and slow organic increases in subscribers won’t solve this problem anytime soon. This is the single greatest argument for a merger between the two, and nothing else can solve this fundamental problem. The fifth company in the mix there is Tracfone, which is a mobile virtual network operator (MVNO), which piggybacks off the carriers’ networks. Most of its costs are variable rather than fixed, and as such it doesn’t have the same scale disadvantages, but it has to pay wholesale rates to the carriers, which doesn’t allow it to be as profitable as AT&T and Verizon either.

As you can see, both T-Mobile and Sprint are languishing in the single digits, while AT&T and Verizon were at around 25% and over 30% respectively last quarter. This is a direct result of their lack of scale, and slow organic increases in subscribers won’t solve this problem anytime soon. This is the single greatest argument for a merger between the two, and nothing else can solve this fundamental problem. The fifth company in the mix there is Tracfone, which is a mobile virtual network operator (MVNO), which piggybacks off the carriers’ networks. Most of its costs are variable rather than fixed, and as such it doesn’t have the same scale disadvantages, but it has to pay wholesale rates to the carriers, which doesn’t allow it to be as profitable as AT&T and Verizon either.

Ultimately, though, the merger faced enormous regulatory opposition, and it was by no means a certainty that it would go through. US regulators would apparently rather see a short-term continuation of the current market structure than a more sustainable long-term competitive environment. I suspect that will come back to bite them a year or two from now. The challenge is that neither Sprint nor T-Mobile is exactly on the brink of collapse today, and so it’s easy to argue the situation isn’t urgent. However, each company faces fundamental challenges beyond those related to scale, and I’ll address those below.

Where does Sprint go from here?

Sprint (or rather its owner, SoftBank) was the driving force behind the merger, and Masa Son clearly felt that combining the two companies was the best way forward for Sprint. As such, Sprint has some big questions to answer in terms of how it moves forward alone.

Sprint suffers from several particular challenges at this point, some of which I covered in my Hesse piece:

- Its current network upgrade program is necessary and important for future growth and competitiveness, but in the short term is causing disruption, poor performance and customer churn. Sprint says that where the upgrade is substantially completed churn improves significantly (slide 9), but in the meantime it’s suffering, and its churn has increased. It’s not helped by the fact that it has several network equipment vendors running different parts of the network, and where they bump up against each other things get particularly complicated.

- Sprint’s brand doesn’t really stand for anything in the market today. Individual campaigns such as the Framily plan are somewhat successful, but they don’t really do anything to build the broader Sprint brand. Sprint’s brand campaigns have focused on taglines such as “Happy Connecting” and “America’s Newest Network” but they don’t convey a specific idea.

- Meanwhile, Sprint lags on LTE coverage, and although it’s closing the gap, it’s doing so slowly and even where it has the network in place it doesn’t perform particularly well.

For all these reasons, Sprint is losing customers and as such moving in the wrong direction in the battle for scale. It seems to have lost its way somewhat in the last year or so, after several years of making decent progress, and I think that stemmed partly from a disconnect between Masa Son and Dan Hesse on a personal level. It’s hinted at in this paragraph from Hesse’s farewell email to Sprint employees but it’s been evident for a while:

A “controlled entity” like Sprint can be most effective when the majority owner and the CEO are fully aligned and are great partners. Marcelo and Masa enjoy an exceptional relationship which has grown out of mutual respect between two very successful entrepreneurs. This is the right time in Sprint’s evolution for Marcelo to take the reins and get the most benefit from our relationship with SoftBank.

With two aggressive entrepreneurial types at the head of Sprint, the chances are that it will move more quickly to address some of Sprint’s challenges, both by reducing costs to increase margins and by lowering prices to win more customers. I almost always advise against competing on price, especially when a company enjoys no cost advantage over competitors and when those competitors have deeper pockets, and I’m wary of a price-focused competitive strategy from Sprint. Its wholesale and connected devices businesses are doing well – Sprint added more subscribers in these two categories than any other US carrier in Q2 – so this should be an area of continued investment for the company. As AT&T pursues almost every new opportunity in wireless (connected homes, connected cars, connected devices) itself, there’s an opportunity for a carrier more focused on enabling third parties to succeed.

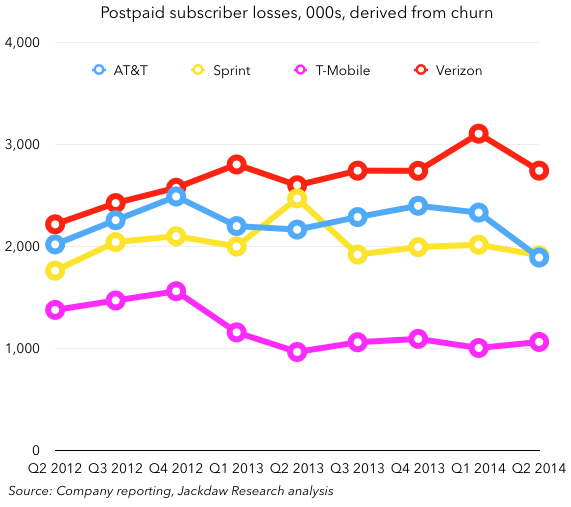

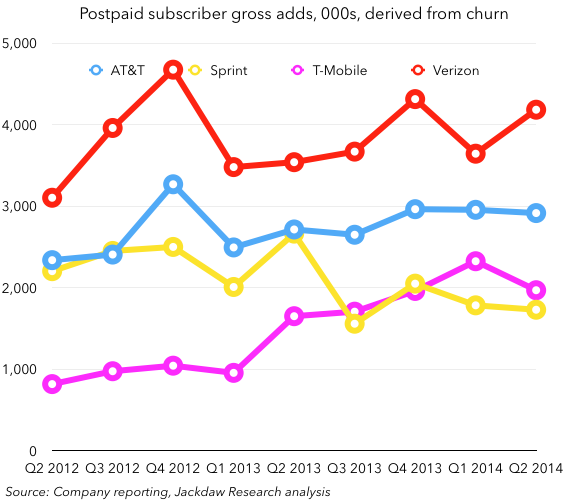

But Sprint fundamentally needs to fix its retail business too, and that has to start with a rapid conclusion to the network upgrade process, pouring more money into it in the short term if necessary to get it done. It’s the single biggest barrier to Sprint’s growth right now and needs to be fixed pronto. Marketing is the other side of the coin. The problem isn’t so much that Sprint is losing more subscribers than its competitors:

But rather that it’s not gaining as many:

But rather that it’s not gaining as many:

And that’s where marketing comes in. Sprint needs to find a niche and positioning in the market where it can truly differentiate itself, and I’m not convinced that it should lead with price. However, as long as it suffers from a network disadvantage and few other obvious advantages, it may have to fall back on price at least on a temporary basis until its network upgrade is complete.

Where does T-Mobile go from here?

Sprint’s owners were openly pursuing a merger, and as such could also be open about Sprint’s need for greater scale. But T-Moble’s leadership has had to be more cautious, and so even though John Legere has repeatedly talked about the benefits of greater scale, he’s also been careful to position T-Mobile’s current trajectory as a sustainable one. So let’s start there.

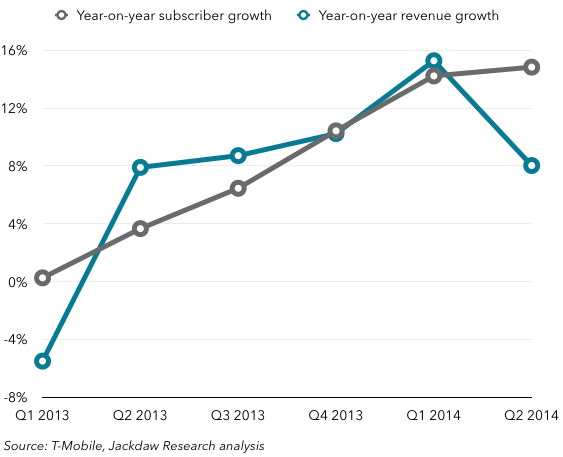

The turnaround at T-Mobile in the last year or so under John Legere has been enormously impressive – he took a carrier which had long since lost its way and arguably suffered from the same branding and marketing problems as Sprint now does and turned it into a thriving, growing carrier which appears to have real momentum. As long, that is, as you measure all these things by growth alone, and not by margins. The chart below shows the impressive growth numbers:

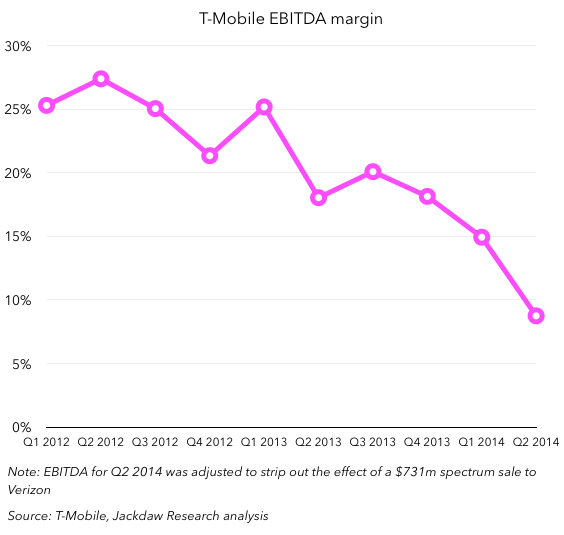

The next chart, though, shows what’s been happening to T-Mobile’s EBITDA margin as it’s embarked on this growth blitz:

The next chart, though, shows what’s been happening to T-Mobile’s EBITDA margin as it’s embarked on this growth blitz:

As you can see, the growth has come at a significant cost in terms of margins, and it’s most clearly seen at the EBITDA level. That’s because almost everything T-Mobile has done to grow its subscribers has involved either spending money or taking less money from customers. The most obvious example is the early termination fees (ETFs) it has been paying off for customers switching from other carriers, but its reduced rates for international calling and roaming are others. At the same time, T-Mobile is investing significantly in its network upgrade program over the last two years, though that spend has tapered off lately, and for that and other reasons T-Mobile’s net margin has remained at close to zero for some time now:

As you can see, the growth has come at a significant cost in terms of margins, and it’s most clearly seen at the EBITDA level. That’s because almost everything T-Mobile has done to grow its subscribers has involved either spending money or taking less money from customers. The most obvious example is the early termination fees (ETFs) it has been paying off for customers switching from other carriers, but its reduced rates for international calling and roaming are others. At the same time, T-Mobile is investing significantly in its network upgrade program over the last two years, though that spend has tapered off lately, and for that and other reasons T-Mobile’s net margin has remained at close to zero for some time now: Note that in Q2 2014, T-Mobile benefited from a $731m spectrum sale to Verizon which boosted all its margins. I was able to strip that effect out of the EBITDA margin chart above, but it’s harder to do that with net margins because of the tax and other implications. As such, readers shouldn’t read too much into that number. In addition, I left off the number for Q3 2012, in which T-Mobile took a huge net loss on a one-off basis. The point is that it has been several quarters since T-Mobile posted a positive net margin without the help of a one-off boost.

Note that in Q2 2014, T-Mobile benefited from a $731m spectrum sale to Verizon which boosted all its margins. I was able to strip that effect out of the EBITDA margin chart above, but it’s harder to do that with net margins because of the tax and other implications. As such, readers shouldn’t read too much into that number. In addition, I left off the number for Q3 2012, in which T-Mobile took a huge net loss on a one-off basis. The point is that it has been several quarters since T-Mobile posted a positive net margin without the help of a one-off boost.

Even the growth has started to slow down lately, though, as you can see in the growth chart earlier. And that’s because T-Mobile didn’t have a new major driver for growth in Q2. This highlighted how little momentum there really is at T-Mobile, and how much each quarter’s growth has been driven by specific actions taken in that quarter. Hence, I suspect, T-Mobile’s new promotional $100 for 10GB shared by four lines. But John Legere’s whole rationale for claiming that T-Mobile can achieve sustainable, profitable growth rests on two assumptions:

- People who come to T-Mobile off the back of its promotions will stay even if competing carriers offer promotions too (i.e. they’re price sensitive enough to switch once but not again)

- At some point, this growth becomes self-sustaining, since T-Mobile can’t afford to keep up the giveaways indefinitely. This relies not only on switchers staying, but on those switchers convincing others to switch too.

My biggest concern about T-Mobile is that I don’t believe either of these assumptions is true. I think the only way T-Mobile can keep up its current rate of growth is to continue funding it with financial incentives, and that in turn is unsustainable from a margin perspective. The problem is that everyone sees T-Mobile’s current growth and apparent success and uses it to argue that it clearly doesn’t need a merger to be successful, which I think is false, at least in the medium to long term.

Other mergers for T-Mobile

There is, of course, still the possibility that someone else will buy T-Mobile, including French carrier Iliad and US satellite operator DISH. But neither of these mergers would solve the fundamental scale problem, and they each come with other baggage. Iliad is suffering from the same delusion that has afflicted many a would-be cross-Atlantic acquirer: namely, that if only they could apply their business practices on the other side of the pond, they’d be enormously successful. The problem is that the markets are geographically, politically and culturally different in ways that limits enormously the applicability of European business models in the US and vice versa. The other challenge with the Iliad offer is that it promises $10 billion in synergies, but the real synergies from cross-border wireless mergers are vanishingly small. T-Mobile is already running very lean (and thin on margins, as we’ve seen) and as such there simply isn’t room to cut costs enormously.

DISH, on the other hand, suffers from a different problem (one which the AT&T-DirecTV merger conversely doesn’t have) and that’s that it leaves a massive hole in the bundle consumers want to buy: wireline broadband. It would provide TV and mobile services, but not home broadband or phone services. The latter is less important, but the former is critical – arguably more so in the long-term than pay TV services – and a combined DISH-T-Mobile wouldn’t be able to offer it. It also offers very few synergies beyond sales and distribution.

T-Mobile as the largest prepaid carrier

T-Mobile made a claim in a press release yesterday which could be seen as misleading in its wording:

the Un-carrier has overtaken rivals AT&T, Verizon and Sprint to become the No.1 U.S. wireless provider in the increasingly important prepaid mobile marketplace

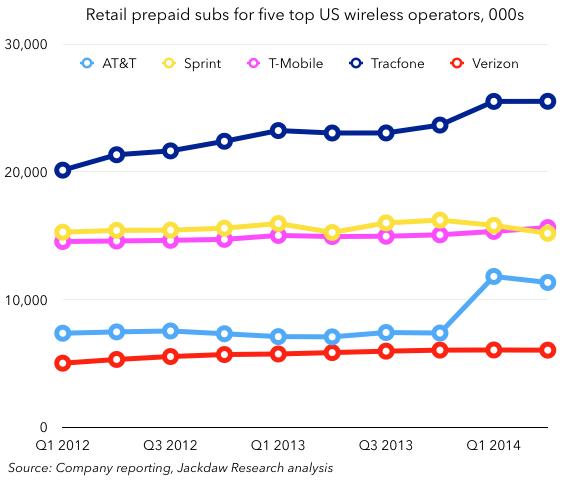

T-Mobile has since clarified to me directly that this sentence was related to operators who run on their own networks, but it’s not at all clear from the press release itself. Look at the real situation below:

Yes, T-Mobile is now the largest US prepaid carrier, but it’s not the largest prepaid wireless provider, to use T-Mobile’s wording. Tracfone is the largest prepaid provider, but isn’t a carrier as such. T-Mobile’s claim rests on that difference but its press release didn’t make that clear.

Yes, T-Mobile is now the largest US prepaid carrier, but it’s not the largest prepaid wireless provider, to use T-Mobile’s wording. Tracfone is the largest prepaid provider, but isn’t a carrier as such. T-Mobile’s claim rests on that difference but its press release didn’t make that clear.

T-Mobile catching Sprint by the end of the year

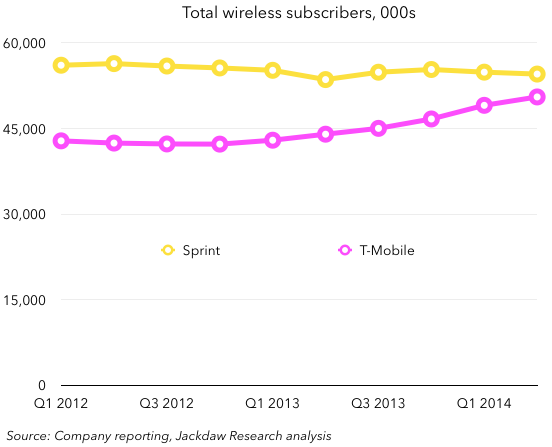

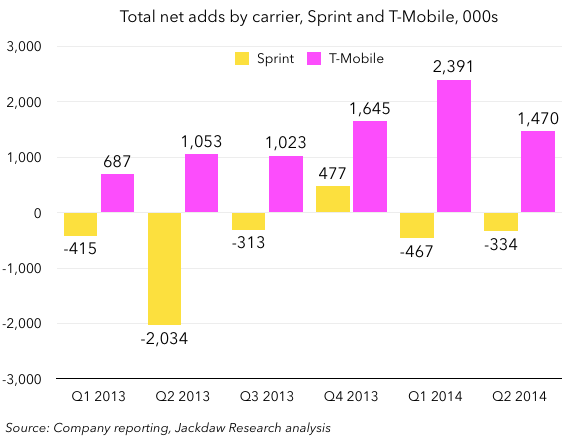

In a stream of tweets yesterday about T-Mobile and Sprint, John Legere predicted that T-Mobile would pass Sprint in total number of subscribers by the end of the year. That’s not an enormously bold claim, but I think it might be a stretch. Here’s what the two carriers’ subscriber numbers have done over the last few quarters:

The companies ended Q2 2014 with 54.553m (Sprint) and 50.545m (T-Mobile) respectively. As the chart shows, the gap has narrowed considerably over the last two years. The chart below shows net adds specifically for each company for the last six quarters:

The companies ended Q2 2014 with 54.553m (Sprint) and 50.545m (T-Mobile) respectively. As the chart shows, the gap has narrowed considerably over the last two years. The chart below shows net adds specifically for each company for the last six quarters: Given that the gap between the two is almost exactly four million subscribers, the two companies have to close the gap by an average of two million for each of the next two quarters. In Q2, the gap only closed by 1.8 million, whereas in Q1 it closed by 2.9 million, so a lot depends on which you think is a better guide to Q3 and Q4. Certainly, looking at the chart above, Q2 looks like a better representation of the longer-term run-rate than Q1, which would suggest Sprint would remain ahead on December 31. But we need to consider what else could change between now and then. T-Mobile’s growth has slowed in the past quarter, and as I discussed above I think it’s recent growth is likely unsustainable over the longer term. In addition, Sprint continues to make progress on its network upgrade, as we also discussed above, and as such should start to see some improvement in churn and net adds as a result.

Given that the gap between the two is almost exactly four million subscribers, the two companies have to close the gap by an average of two million for each of the next two quarters. In Q2, the gap only closed by 1.8 million, whereas in Q1 it closed by 2.9 million, so a lot depends on which you think is a better guide to Q3 and Q4. Certainly, looking at the chart above, Q2 looks like a better representation of the longer-term run-rate than Q1, which would suggest Sprint would remain ahead on December 31. But we need to consider what else could change between now and then. T-Mobile’s growth has slowed in the past quarter, and as I discussed above I think it’s recent growth is likely unsustainable over the longer term. In addition, Sprint continues to make progress on its network upgrade, as we also discussed above, and as such should start to see some improvement in churn and net adds as a result.

On the other hand, Q3 and Q4 are big upgrade quarters, with the new iPhone(s) likely to launch right at the end of Q3 and continue to be a huge seller in Q4, and the holiday season spurring huge sales in Q4 too. Sprint and T-Mobile both saw 9% of their postpaid base upgrade in Q4 last year, so a good set of upgrades for either company could make a huge difference. Both have the iPhone now, but T-Mobile has been running its Test Drive campaign, which may drive higher iPhone net adds in Q3 and Q4, but it isn’t likely to make a huge difference. However, the iPhone is newer at T-Mobile than at Sprint, so there may be a higher number of customers looking to pick up their first iPhone.

Overall, I think it’s too close too call for certain, but on balance I think it’s unlikely that T-Mobile will catch Sprint by the end of the year, especially if Sprint gets more aggressive on price or on marketing. But it’ll be a fun race to watch in the meantime!

Pingback: Sprint Kills Off the Framily Plan, but May Keep the Frobinsons Around – AdAge.com | Everyday News Update()

Pingback: Sprint Kills Off the Framily Plan, but May Keep the Frobinsons Around |()

Pingback: Sprint Kills Off the Framily Plan, but May Keep the Frobinsons Around | Report News Today()

Pingback: The Net Press Sprint Kills Off the Framily Plan, but May Keep the Frobinsons Around – AdAge.com | The Net Press()