Note to new readers: This is part of a series on major tech companies’ Q3 2014 earnings. Prior analysis on Amazon can be seen here.

Last quarter I did a pretty deep dive on Amazon and many of its financial metrics, and specifically addressed the question of how sustainable its business is, and whether it’s really realistic to expect it to be able to turn on the “profit spigot” at some point in the future. This quarter I’m taking a simpler, more focused approach on the cost of growth, the pursuit of which is the core reason Amazon is losing money.

Hiring at a fierce rate

Amazon’s hiring new employees at a fierce rate. This is one of the two primary costs of having a very logistics-heavy business, and the key driver behind Amazon’s investments in robotics. But for now the company still needs lots and lots of people to staff fulfillment centers around the world. Here’s are several charts showing statistics related to the number of employees:

As you can see, the growth is enormously rapid. I pointed out yesterday in a tweet that Amazon hired more than twice as many employees just in the past quarter than Facebook has employees overall. They’re obviously very different businesses, but this just highlights quite how people- and infrastructure-intensive Amazon’s business is. Amazon has now reached a rate of 40,000 net new employees per year, which is astonishing when you consider it only employed 40,000 in total back in 2011:

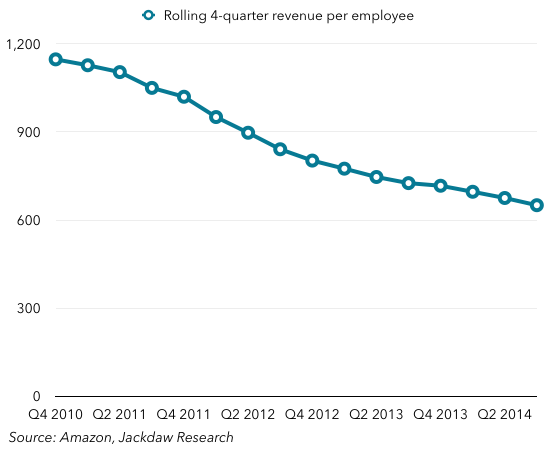

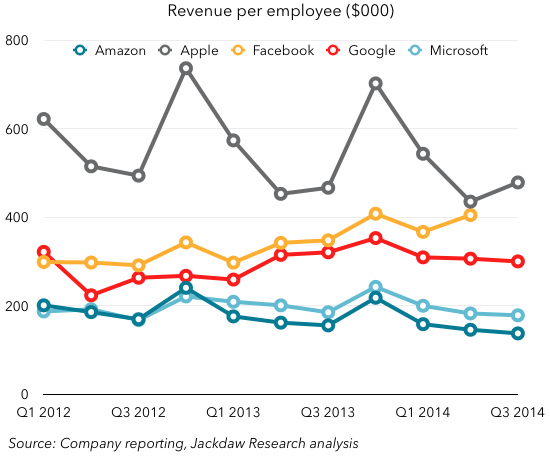

The other thing about Amazon which is different from many of its major competitors is that the kind of people who make up the employee ranks are very different. At Amazon they’re generally far less skilled and therefore much cheaper to employ, which means that it can afford to drive far less revenue per employee than companies such as Apple, Microsoft and Google, which employ a much more expensive mix of employees:

Here are the comparative numbers for other major tech companies (Facebook hasn’t reported yet):

Investing in infrastructure

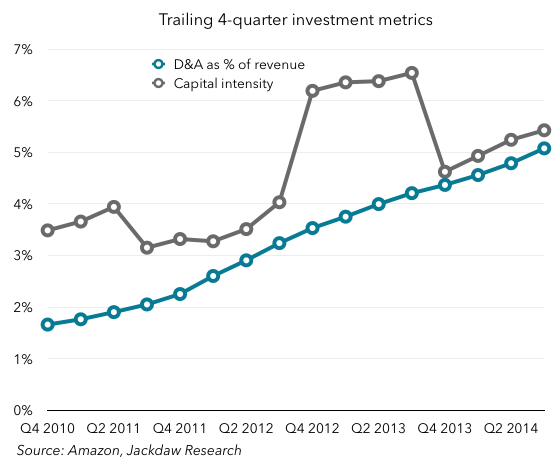

The other major investment Amazon has to make, of course, is in infrastructure, in two major flavors: fulfillment centers and cloud servers and the like to support AWS. There’s also a third, smaller infrastructure investment in digital content delivery. But Amazon has invested hugely in each of these over the last few years and continues to do so, which is a major reason for the decline in profitability. I’ve shared versions of this chart before, but here is trailing 4-quarter depreciation and amortization as a % of revenues, and capital intensity on the same basis (capex as a % of revenues):

You can see that (barring the blip in 2012 from a major investment in property) the two lines are trending steadily upwards. Depreciation and amortization (the best reflection in operating costs of all this investment) is now 5% of revenue, from under 2% back in 2010, and capital intensity has been over 5% for a few quarters now. That’s the biggest use of the company’s cash, along with payments on leases, and the combined number is rising steadily as a percentage of revenues. Though Amazon doesn’t break down its capital spending by region, it’s interesting to look at its profitability by region as a signal of where all this money is going:

You can see that (barring the blip in 2012 from a major investment in property) the two lines are trending steadily upwards. Depreciation and amortization (the best reflection in operating costs of all this investment) is now 5% of revenue, from under 2% back in 2010, and capital intensity has been over 5% for a few quarters now. That’s the biggest use of the company’s cash, along with payments on leases, and the combined number is rising steadily as a percentage of revenues. Though Amazon doesn’t break down its capital spending by region, it’s interesting to look at its profitability by region as a signal of where all this money is going:

As you can see, both Amazon’s two geographies have seen falling margins, but the international business is the real drag on overall margins, as it’s been unprofitable for all but a couple of quarters in the past two years. This is likely because of both heavy investment in infrastructure in these markets, particularly key strategic markets like China and India, and also perhaps more aggressive pricing to get customers hooked in those markets. The cost of opening up in entirely new markets and expanding in smaller markets is also a lot higher than in mature markets, and fraught with risk. In the US, where Amazon already has a huge fulfillment infrastructure, building more can be entirely success driven and is about getting fulfillment centers closer to existing customers. In these new markets, much of the construction comes before the spending it will support, and some of that spending may not come for some time.