Note: This is part of a series on major tech companies’ Q2 2014 earnings (e.g. Google here, Microsoft here, Apple here and here, Netflix here and Facebook here). My post about Amazon’s earnings last quarter is here.

AWS in trouble

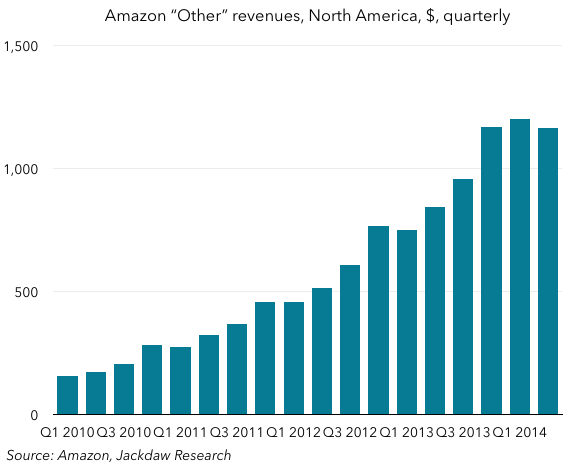

Much has been said already about the fact that Amazon Web Services (AWS) seemed to do poorly this quarter, compared with previous quarters. We don’t know exactly how it did, because this is one of the many things Amazon doesn’t report directly, but the best proxy we have is the Other category, especially in North America, so here’s that number:

As you can see, after lots of quarters of good growth, revenues suddenly dipped in the second quarter over the first quarter, which they’ve never done before, and year on year growth dropped from over 60% in most recent quarters to 38.4%. Bear in mind, too, that there are other components to this Other bucket, including advertising, which is an increasingly important (and rapidly growing) segment for Amazon. That may well mean that AWS revenues performed even more poorly than the Other segment as a whole.

As you can see, after lots of quarters of good growth, revenues suddenly dipped in the second quarter over the first quarter, which they’ve never done before, and year on year growth dropped from over 60% in most recent quarters to 38.4%. Bear in mind, too, that there are other components to this Other bucket, including advertising, which is an increasingly important (and rapidly growing) segment for Amazon. That may well mean that AWS revenues performed even more poorly than the Other segment as a whole.

Margins – what’s really going on

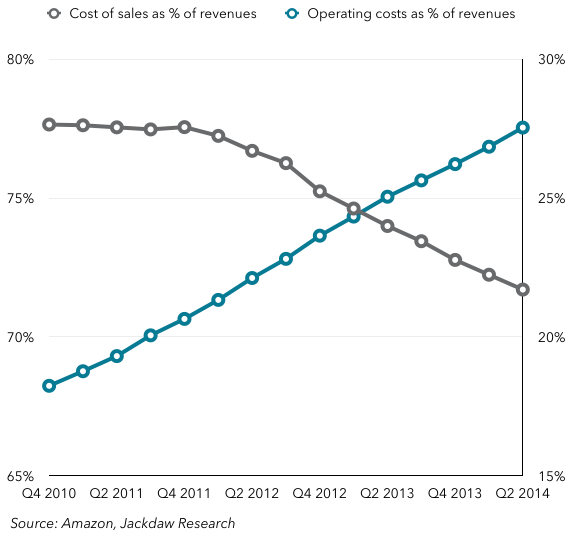

Amazon’s margins are the butt of jokes every quarter, but little of the coverage ever really looks at what’s going on behind the numbers. So I wanted to do a deeper dive than I have before on what exactly has been going on with Amazon’s margins over the last several years. Simply put, there are a number of inputs to the operating income output, and they’re not all moving in the same direction. Here’s an overview of what’s happened to two of the major components of Amazon’s operating costs over the last several years (on a trailing 4-quarter basis):  What you’ll see is that the cost of sales has been steadily declining as a percentage of revenues, but all other operating costs combined have been rising even more rapidly as a percentage of revenues. Cost of sales is the cost of the goods sold, whether physical goods or the content Amazon sells through its digital channels, as well as the cost of shipping physical goods to customers. Other operating expenses include Fulfillment (e.g. the costs of running fulfillment centers); Marketing; Technology and Content (which is the cost of running the infrastructure that delivers Amazon’s digital content services and AWS); and General and Administrative (which is mostly payroll and related costs for employees not included in the other two buckets and is small). A breakdown of some of these other categories is shown in the next chart, along with Shipping costs which are part of Cost of Sales:

What you’ll see is that the cost of sales has been steadily declining as a percentage of revenues, but all other operating costs combined have been rising even more rapidly as a percentage of revenues. Cost of sales is the cost of the goods sold, whether physical goods or the content Amazon sells through its digital channels, as well as the cost of shipping physical goods to customers. Other operating expenses include Fulfillment (e.g. the costs of running fulfillment centers); Marketing; Technology and Content (which is the cost of running the infrastructure that delivers Amazon’s digital content services and AWS); and General and Administrative (which is mostly payroll and related costs for employees not included in the other two buckets and is small). A breakdown of some of these other categories is shown in the next chart, along with Shipping costs which are part of Cost of Sales:

What you can see is that all of these except Shipping has been rising over this period, with shipping remaining fairly flat through 2012 and early 2013 and rising only slightly in the last few quarters. The steepest rises are in Fulfillment, which went from 8.5% to 11.8% over the period, and Technology and Content, which went from 5.1% to 9.6%. Shipping and Fulfillment are somewhat related – as Amazon invests in Fulfillment Centers closer to customers, it pays less in Shipping. Technology and Content is likely highly driven by AWS investments. In essence, though, Amazon has been largely investing in the infrastructure that delivers its two major products: e-commerce and AWS. This is also reflected in its capital expenditures and in its depreciation and amortization expense, which are also rising when expressed as a percentage of revenues:

What you can see is that all of these except Shipping has been rising over this period, with shipping remaining fairly flat through 2012 and early 2013 and rising only slightly in the last few quarters. The steepest rises are in Fulfillment, which went from 8.5% to 11.8% over the period, and Technology and Content, which went from 5.1% to 9.6%. Shipping and Fulfillment are somewhat related – as Amazon invests in Fulfillment Centers closer to customers, it pays less in Shipping. Technology and Content is likely highly driven by AWS investments. In essence, though, Amazon has been largely investing in the infrastructure that delivers its two major products: e-commerce and AWS. This is also reflected in its capital expenditures and in its depreciation and amortization expense, which are also rising when expressed as a percentage of revenues:

Capital expenditure looks very strange in the above chart, but it’s highly driven by spikes in a few quarters, especially the third quarter of each year, likely to ramp up capacity for the big fourth quarter. Nevertheless, the overall trend in both numbers is clearly up and to the right. Amazon is spending more than it ever has on capital investments. Capital spending is dominated by purchases and leases of property and equipment, with only a tiny proportion going on software and website development.

Capital expenditure looks very strange in the above chart, but it’s highly driven by spikes in a few quarters, especially the third quarter of each year, likely to ramp up capacity for the big fourth quarter. Nevertheless, the overall trend in both numbers is clearly up and to the right. Amazon is spending more than it ever has on capital investments. Capital spending is dominated by purchases and leases of property and equipment, with only a tiny proportion going on software and website development.

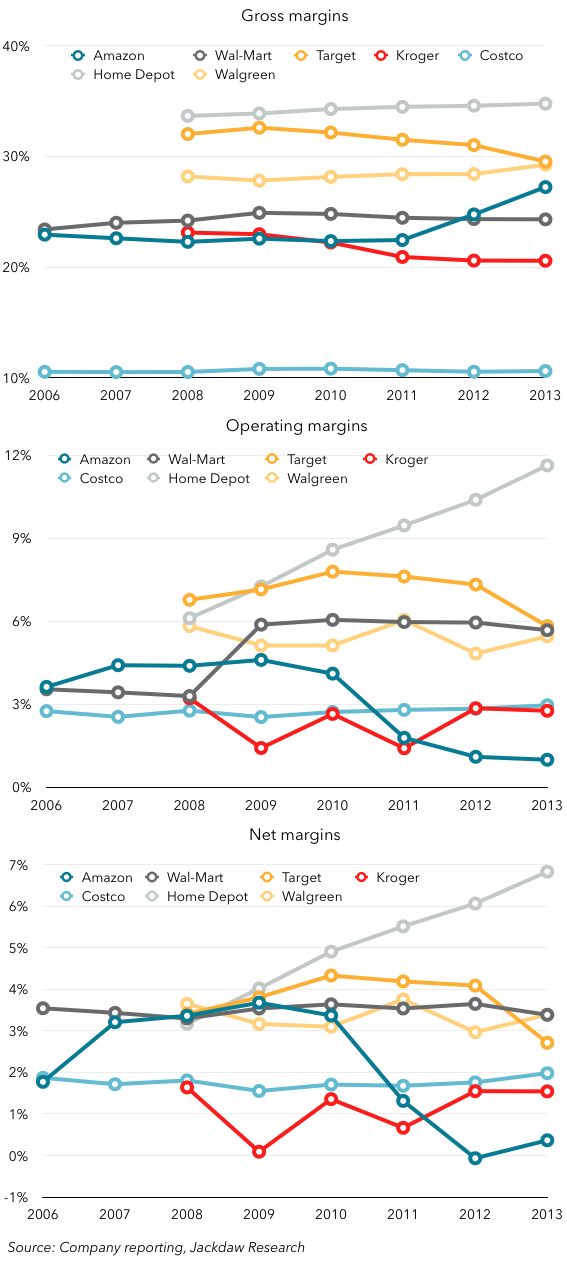

To make a long story short, Amazon’s operating costs have been rising rapidly as it invests in this infrastructure. But to offset that increase, it has been steadily expanding its gross margin, to maintain operating margins at roughly 1% until very recently. AWS, which has far higher gross margins than the rest of Amazon’s business, is likely responsible for much of the improvement in Amazon’s gross margins. See this comparison with other retailers to see how AWS is changing Amazon’s business:

Amazon’s margins had been very similar to those of other low-cost retailers like Costco and Walmart. But over the last few years, gross margins have risen and operating and net margins have fallen. Amazon’s margin profile is looking less and less like a retailer. However, it’s not yet looking anything like a big, successful consumer technology company:

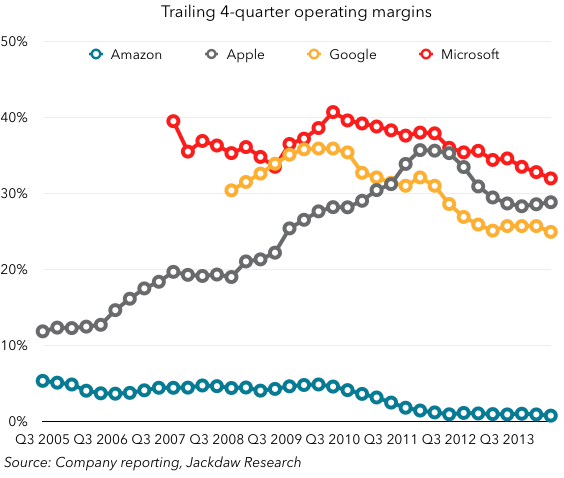

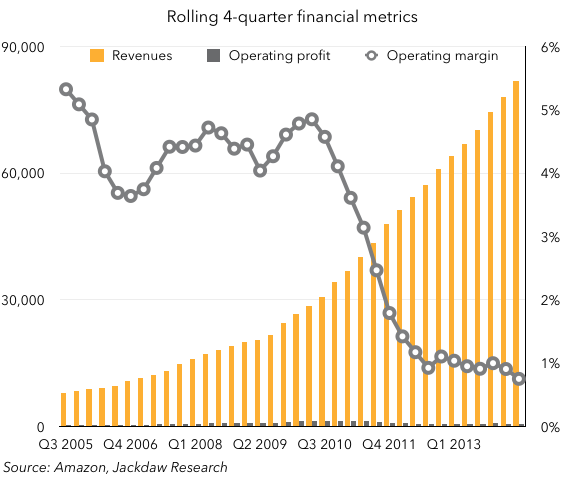

Amazon continues to be an enormous anomaly in the consumer technology market. A company that grows extremely rapidly but doesn’t generate anything like the margins of its closest competitors. Look at this long-term view of Amazon’s revenue growth and margins:

Turning on the profit spigot

Turning on the profit spigot

The question everyone always asks about Amazon is to what extent is it possible for Amazon to turn on the profit spigot at some point, sacrificing high growth rates for better margins. The biggest problem with this is that Amazon is still first and foremost a retailer, with retailer margins. AWS is helping a bit, but if that continues to struggle as it did this quarter, it may not make as big a dent as some have hoped. As price competition intensifies in the cloud services market, margins will start to come down too. But Amazon’s ability to claw its way out of 1% margins is going to be dramatically constrained by its focus on e-commerce. Raising prices is really the only way to raise gross margins in the retail business, but the price you pay for being a low-cost retailer is very little pricing flexibility.

When it comes to operating margins, all Amazon’s metrics are going in the wrong direction. Not only are its physical and digital delivery costs expanding more rapidly than revenues, but Marketing costs are rising too, as Amazon has to fight harder to win business. Yes, Amazon could stop investing as heavily in infrastructure for physical delivery, but its current infrastructure is enormously biased towards the US:

If Amazon wants to continue to grow in major regions like China and Europe, it’s going to have to expand fulfillment center capacity significantly from current levels. The US is already dominating growth for Amazon, and that trend would only accelerate:

If Amazon wants to continue to grow in major regions like China and Europe, it’s going to have to expand fulfillment center capacity significantly from current levels. The US is already dominating growth for Amazon, and that trend would only accelerate: No-one but Amazon knows what it has planned for its long-term future, but I’m increasingly skeptical that it will ever be possible for Amazon to crank up margins without significantly impacting growth, especially as long as its results are dominated by e-commerce.

No-one but Amazon knows what it has planned for its long-term future, but I’m increasingly skeptical that it will ever be possible for Amazon to crank up margins without significantly impacting growth, especially as long as its results are dominated by e-commerce.