Amazon filed its 10-K report for 2016 late last week, and it adds a few bits of additional information which haven’t been in previous versions. Most notably, it provides a breakdown of revenue by similar product, which is the first real visibility we’ve had into Prime and certain other categories. It doesn’t report Prime directly, but there’s enough data here to provide some really interesting insights into the Prime program, how many members it has, how much revenue it generates, and how revenue is split between shipping and other services.

Amazon’s new revenue breakdown

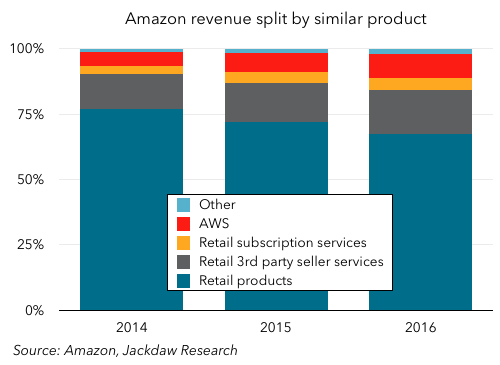

First up, here’s the new breakdown. Revenue is split into five categories which, other than AWS, we haven’t seen broken out before:

- Retail Products – this is basically all e-commerce plus most one-off sales of digital goods except those which are sold on a net basis (likely mostly apps); plus any direct shipping revenue associated with e-commerce purchases

- Retail third-party seller services – this is all the revenue Amazon generates from its third party sellers including commissions, related fulfillment and shipping fees

- Retail subscription services – Prime is the biggest component here, but it also includes Audible, Amazon Music, Kindle Unlimited, and other non-Prime subscriptions

- AWS – Amazon Web Services, as reported in its segment reporting

- Other – all the stuff that doesn’t fit in any other bucket, with co-branded credit cards and advertising the only two components called out specifically.

Here’s what that revenue breakdown looks like in percentage terms over the last three years:

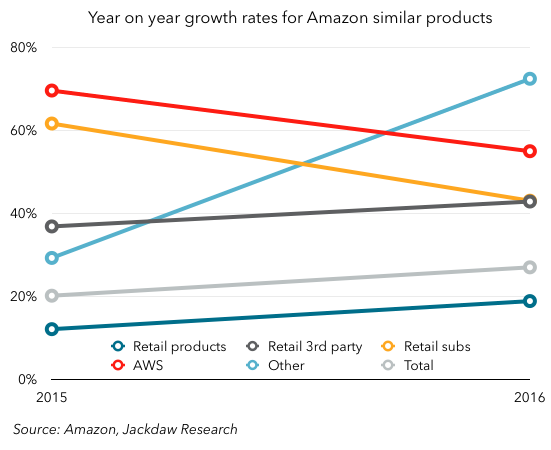

As you can see, Product Sales are by far the largest component, but they’re falling rapidly as a percentage of the total, from 77% in 2014 to 67% in 2016, while the other categories are coming up fast. Here are the growth rates for the last two years for these various components:

As you can see, the growth rates are all over the map, with the fastest-growing that mysterious Other section, which I suspect is largely driven by Amazon’s small but flourishing ad business. eMarketer estimates that this is already a roughly billion-dollar business for Amazon, so that would make sense, though the growth rate here is much higher than eMarketer projects. Those credit cards must be doing well too.

But outside that, it’s worth noting that third party services are growing much faster than product sales, with retail products (i.e. Amazon’s own direct sales) the slowest growing of any of these categories. Both retail subscriptions and AWS are coming down somewhat in percentage growth terms, but largely as a factor of becoming quite big numbers – in both cases, the dollar growth year on year actually increased. That third party sellers are growing faster than first party is actually a good thing – Amazon’s margins on those services are much higher, because it only reports its cut rather than the gross take as revenue. This growth has been a major driver, alongside AWS, of Amazon’s increasing margins lately.

Deducing Prime subscribers

Let’s focus, though, on that retail subscriptions business, because that’s where Prime revenue sits. We need to make some assumptions about how much of that revenue is actually Prime to start. Morgan Stanley reckons it’s about 90%, and though I was originally tempted to say it was more than that, checking into the size of Audible made me think it’s probably about right. So I’m going to stick with that.

If we want to know subscriber numbers, though, we need to figure out what the average subscriber pays, and that’s a complex proposition because the price of Prime increased by $20 in 2014 in the US, and costs different amounts in each market. If we make reasonable assumptions about the mix of where those Prime subscribers are located (e.g. by using Amazon’s revenue split by country) and then apply the going rates at various times for a Prime subscription, we can arrive at a reasonable average. Mine starts at $76 in 2014 and rises to $81 in 2015 and $82 in 2016, whereas Morgan Stanley’s is at $88 for both 2015 and 2016.

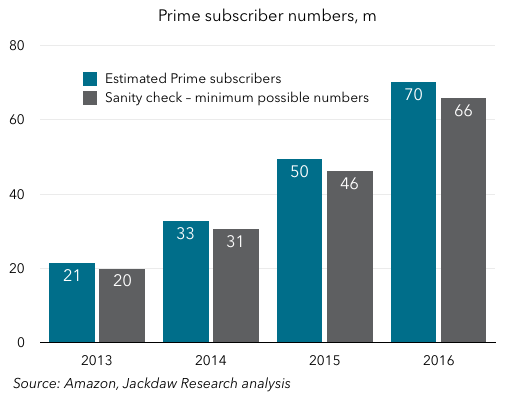

On that basis, then, here’s a reasonable estimate for Prime’s subscriber numbers over the last four years, together with a sanity check in the form of the minimum possible number Amazon might have based on various public statements it’s made:

The numbers you end up with are just barely above those minimum numbers provided by Amazon. There’s no way to be 100% sure about my numbers, but they certainly imply that Amazon has been making the biggest possible deal out of its total number ever since that “tens of millions” comment at the end of 2013 (which referred to 21 million subscribers according to my estimate). These numbers would also help explain why Amazon didn’t provide a percentage growth number at the end of 2016 as it did in the previous two years: the percentage likely went down, again as a result of an increasingly large base, not lower subscriber growth – it added 20 million subs in 2016 versus 17 million in 2015.

Prime revenue allocation

One other interesting wrinkle which I’ve wondered about for a long time is the way Amazon allocates revenue between the components of its Prime service, which after all combines free two day shipping with a Netflix-like video subscription and various other benefits. Its financial reporting has always made clear that it allocates these portions of revenue to different buckets – specifically, its Net Product Sales and Net Service Sales categories – even though they all come from the same Prime subscriptions. Understanding this split may seem of purely academic interest, but in fact it’s key to divining the economics of Amazon’s Prime video business.

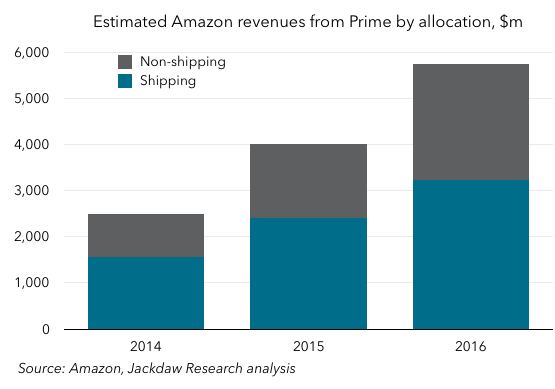

One interesting thing about the new grouping of revenues Amazon provided in its 10-K is that there is just one portion of revenue allocated differently here from in Amazon’s other reporting, and that’s the shipping component of Prime revenues. In the Net Product/Service Sales split, shipping goes into Product, whereas in the Similar Products split it goes into retail subscriptions. Therefore, if we look at the differences between the amounts reported in the various segments, we can deduce the Prime shipping component, and by implication the portion allocated to everything else (mostly video).

What you can see is that the revenue allocation is shifting quite significantly over time from shipping towards the rest – shipping was 63% or almost two thirds of the total in 2014, but only 56% of the total in 2016, and the actual numbers have both risen considerably. For comparison’s sake, the Prime shipping allocation is around a third of Amazon’s total shipping revenue.

Competing with Netflix on content will be tough at these levels

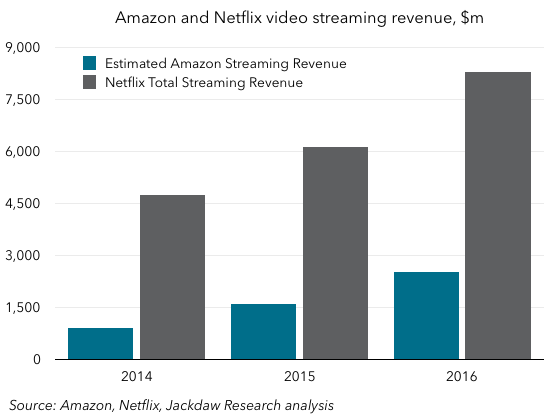

We can then compare Amazon’s non-shipping revenue (the vast majority of which should probably be seen as video revenue) against Netflix’s global streaming revenue:

What you see here is that Netflix’s revenue from its streaming business is massively larger, not least because it allocates the full $8-10 per month it collects from its nearly 100 million subscribers to streaming, whereas even with 70 million subscribers, Amazon only allocates just under half to streaming.

This has significant implications for the viability of the two companies’ investments in original content. Netflix has committed to spending $6 billion in total on content in 2017, which is more than twice Amazon’s entire revenue from streaming video in 2016. To the extent that Amazon wants to be competitive in content, it either needs to lose money on the whole thing as a subsidy for its e-commerce business, or charge (or allocate) a lot more of its total take to streaming video. Interestingly, the standalone monthly Prime Video service Amazon offers comes in at $9, suggesting that without the flywheel benefits of free shipping, it needs to recoup far more like the total real cost of providing the streaming service.

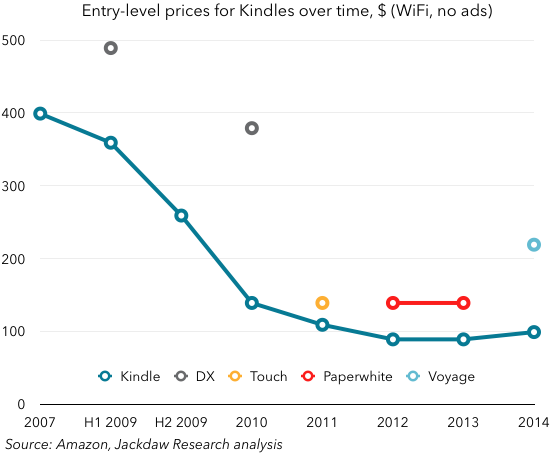

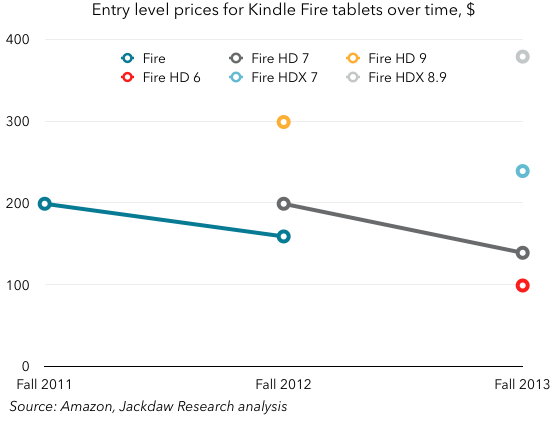

It’s no wonder that there was a slew of articles in late 2011 asking when Kindles would be free, or predicting that they certainly would be shortly (see

It’s no wonder that there was a slew of articles in late 2011 asking when Kindles would be free, or predicting that they certainly would be shortly (see  The trend here is harder to spot, because Amazon hasn’t stuck with a single model throughout the history, rather introducing a series of new models over time. But you can see two distinct trends: individual models have come down in price over time (in the case of the original Fire and the HD 7), while new versions are being introduced at higher prices, actually raising the upper price over time. Amazon has lowered the entry-level price (and you very much get what you pay for at that level) but it’s also moving up the stack into the premium space. The highest base-level price has moved from $200 to $300 to just under $400 over this time.

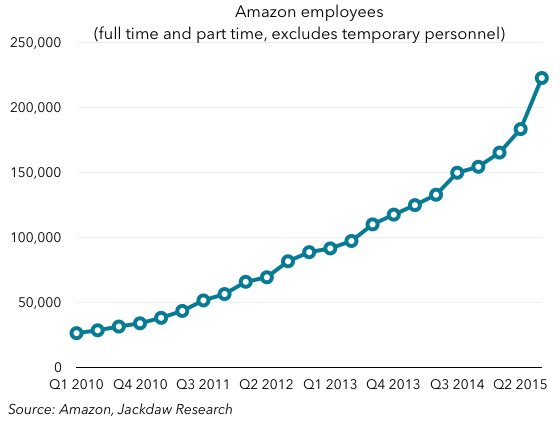

The trend here is harder to spot, because Amazon hasn’t stuck with a single model throughout the history, rather introducing a series of new models over time. But you can see two distinct trends: individual models have come down in price over time (in the case of the original Fire and the HD 7), while new versions are being introduced at higher prices, actually raising the upper price over time. Amazon has lowered the entry-level price (and you very much get what you pay for at that level) but it’s also moving up the stack into the premium space. The highest base-level price has moved from $200 to $300 to just under $400 over this time.