One of the things that struck me the most about Amazon’s earnings last quarter was the rate at which it’s hiring, as that rate has always been high, but accelerated significantly this past quarter. Below, I’m going to share a few key charts to illustrate this trend.

These charts are taken from the slide deck for Amazon I put together each quarter as part of the Jackdaw Research Quarterly Decks Service, a subscription service which provides slides on financial and operating metrics on some major consumer technology companies each quarter. I’ll post a screenshot of the slides in the Amazon deck, which went out to subscribers last night, at the bottom of this post. Any reporters reading this can contact me directly to receive copies of this and other decks from the service.

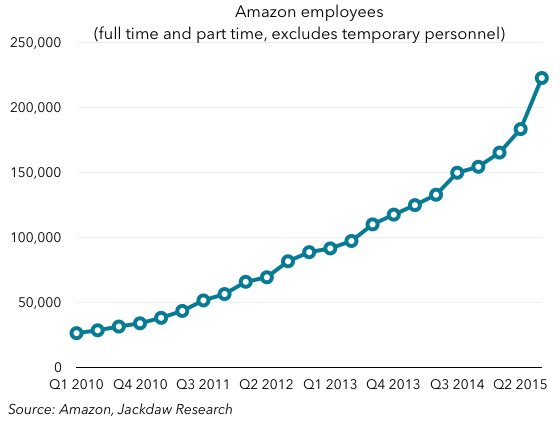

The first chart is the total number of Amazon employees, which includes both full-time and part-time employees, but excludes contractors and temporary personnel, of which Amazon hires many each holiday season: You can see the broad upward trend, but hopefully you can also see the spike this past quarter, which was significantly higher than in previous quarters. To put it in context, let’s look at another couple of charts. The first shows year on year net employee growth and the second shows quarter-on-quarter growth:

You can see the broad upward trend, but hopefully you can also see the spike this past quarter, which was significantly higher than in previous quarters. To put it in context, let’s look at another couple of charts. The first shows year on year net employee growth and the second shows quarter-on-quarter growth:

As you can see, in both cases the growth this quarter was well above the historical trend. So what happened? Well, Amazon’s management was asked about this on the call and this was the answer, from Brian Olsavsky, the CFO (as reported by Seeking Alpha):

As you can see, in both cases the growth this quarter was well above the historical trend. So what happened? Well, Amazon’s management was asked about this on the call and this was the answer, from Brian Olsavsky, the CFO (as reported by Seeking Alpha):

Headcount was up 49% year-over-year, which is higher than Q2 – we saw in Q2. This is going to be primarily in our ops area. If you exclude ops-related employees, our headcount’s growing actually slower than our FX neutral growth rate of 30%. So, what’s going on in ops is we’ve added 14 net fulfillment centers this year, bringing the total to 123 globally. We’ve added four sort centers in the U.S., bringing U.S. footprint to 23. We’re staffing earlier in those locations, we’re in good shape for the holidays and ready to go.

The other issue is there, the other reason is that we are also doing a lot of conversion of temp workers to full-time workers purposefully. There is a metric employment of full-time hires. So it is a little bit higher due to that program.

The bold text there is mine, because it highlights the major drivers here:

- Amazon is building large numbers of new fulfillment centers

- It’s getting those fulfillment centers staffed up to full levels earlier, especially in preparation from the holiday season

- It’s also converting a higher number of the temporary workers it hires to permanent workers.

All this is particularly interesting in light of the recent New York Times story on Amazon’s working conditions (mostly in office jobs), because this is an unprecedented hiring spree at Amazon, but it’s almost all going into “ops” – or fulfillment and other blue-collar jobs. Indeed, this is reflected in Amazon’s rapidly falling revenue per employee: Whereas five years ago Amazon generated over a million dollars per employee, today, it generates less than half that, at $555,000 per employee in Q3 2015, and falling fast. Both the sheer number of employees Amazon has, and the nature of those employees, continues to be one of the biggest differences between Amazon and its business model and all the other big consumer technology companies it competes with. Amazon added 72,900 employees over the last 12 months, which is around 80% of Apple’s total workforce, for comparison’s sake.

Whereas five years ago Amazon generated over a million dollars per employee, today, it generates less than half that, at $555,000 per employee in Q3 2015, and falling fast. Both the sheer number of employees Amazon has, and the nature of those employees, continues to be one of the biggest differences between Amazon and its business model and all the other big consumer technology companies it competes with. Amazon added 72,900 employees over the last 12 months, which is around 80% of Apple’s total workforce, for comparison’s sake.

Here’s that screenshot of the Amazon slide deck from the Jackdaw Research Quarterly Decks service:

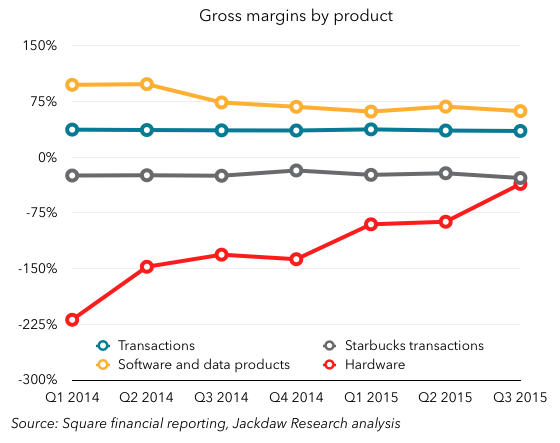

Software and Data Products have had by far the highest margins of all, although they’ve come down as Square has begun to incur costs of revenue around these businesses, which started out at almost 100% margins, with almost no costs. However, the Hardware business has historically been run at a loss, as Square essentially gave away many of its hardware products for free, although it’s now moving to a sell-at-cost model for some of its newer products. Lastly, you can see the huge discrepancy between the gross margins on Starbucks transactions, which have been consistently negative (around 20-30%), and all other transactions, which are very consistent at 35%.

Software and Data Products have had by far the highest margins of all, although they’ve come down as Square has begun to incur costs of revenue around these businesses, which started out at almost 100% margins, with almost no costs. However, the Hardware business has historically been run at a loss, as Square essentially gave away many of its hardware products for free, although it’s now moving to a sell-at-cost model for some of its newer products. Lastly, you can see the huge discrepancy between the gross margins on Starbucks transactions, which have been consistently negative (around 20-30%), and all other transactions, which are very consistent at 35%.