AT&T this morning held a conference for financial analysts in Dallas, at which it outlined both its strategy and its financial guidance following the closing of the acquisition of DirecTV a few weeks ago. The event was live-streamed, and the slides from the various presentations are available to download from this page (where I assume a replay of the conference will be available shortly too). In this piece, I’ll share my thoughts in some depth about some of the key announcements, and briefly hit a few highlights on some other items towards the end, before wrapping up with my conclusions on the prospects for the new AT&T.

Note: for broader context on the TV business that’s central to much of what’s below, see my post yesterday on cord cutting, which provides subscriber growth trends for the largest US pay TV providers.

Putting the new AT&T in context

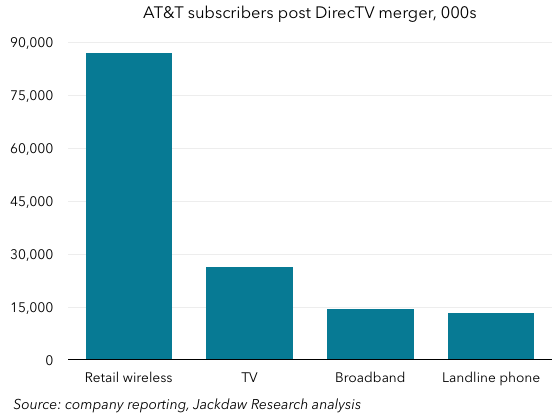

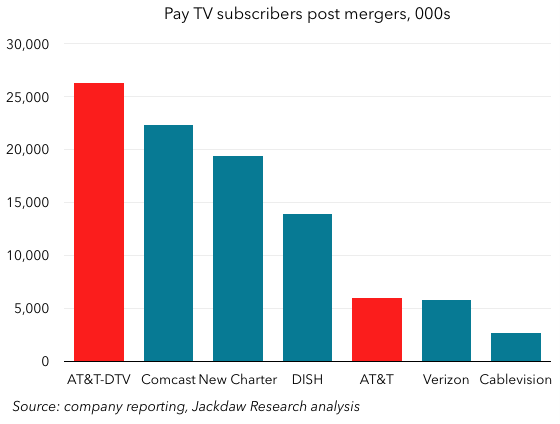

Firstly, I think it’s useful to put the new AT&T in context, among the other large players it competes against. Here is the combined subscriber count for AT&T in the various retail categories it competes in (note that I’ve used retail wireless subscribers, which excludes connected cars, MVNO subscribers and other categories where AT&T isn’t selling directly to end users): As you can see, this is a formidable company at this point, with large numbers of subscribers across these different categories, with wireless by far the largest base. Verizon is the largest carrier by retail subscribers, with around 110 million, putting AT&T second, and far ahead of T-Mobile and Sprint. But in pay TV, AT&T is now the leader in both the US and the world, a dramatic change from its former position (note that “New Charter” represents the combined subscribers of Charter, Time Warner Cable, and Bright House following their merger, if successful):

As you can see, this is a formidable company at this point, with large numbers of subscribers across these different categories, with wireless by far the largest base. Verizon is the largest carrier by retail subscribers, with around 110 million, putting AT&T second, and far ahead of T-Mobile and Sprint. But in pay TV, AT&T is now the leader in both the US and the world, a dramatic change from its former position (note that “New Charter” represents the combined subscribers of Charter, Time Warner Cable, and Bright House following their merger, if successful): This combined scale, at almost five times AT&T’s previous standalone scale, is one of the two key benefits from the merger, and is something I’ll come back to below.

This combined scale, at almost five times AT&T’s previous standalone scale, is one of the two key benefits from the merger, and is something I’ll come back to below.

Cost synergies are significant, especially around content

The true definition of synergy is when two things come together and are greater than the sum of their parts, whereas the term is often used to mean cost savings that result when two things come together (indeed, AT&T talked up $2.5 billion of run-rate synergies from this deal, and that was entirely about cost synergies). However, AT&T also talked about the positive synergies that would come from putting these two businesses together, and they gave us some very interesting specifics around these.

On the cost synergy side, there are two major categories – content and operations. The content savings will come largely from the fact that AT&T can now leverage that combined scale in content buying – John Stephens (AT&T’s CFO) said during the conference that AT&T’s U-verse customers cost $17 per sub per month more for TV content than DirecTV’s customers. That obviously presents huge opportunities for reducing spend on content over time, and those savings make up a good chunk of the overall synergies. The other big chunk comes largely from consolidating operations across the two companies, getting to a single installation model and so on.

Revenue synergies could be far greater

However, to my mind the revenue synergies are much more interesting, and we got some interesting detail there too. AT&T broke out some of the cross-selling and up-selling opportunities as follows:

- Of the 57 million households AT&T passes with its broadband service today, only 13 million have U-verse, and only about half could receive U-verse TV, whereas all 57 million could be sold TV now as part of a bundle from AT&T

- 15 million households have DirecTV but aren’t AT&T Mobility subscribers, and so could be sold mobile services from AT&T

- 21 million AT&T Mobility subscribers don’t take TV from either DirecTV or AT&T today, and so could be sold TV services

- 3 million households in AT&T’s landline footprint have DirecTV but not AT&T broadband.

I’m actually somewhat skeptical of the benefits of a double play that simply combines TV and wireless, because it’s missing the broadband piece. As such, the two middle bullets there seem less compelling to me than the other two, which both involve a more traditional (and likely more appealing) bundle of TV and broadband. Landline/wireless bundles have never been popular, in part because they tend to offer small cost savings and little integration and in part because they make for very high monthly bills that many consumers would rather take in two chunks. In addition, the value proposition of a bundle that offers everything but broadband is not that appealing when customers still have to go to the local cable company for broadband, and are likely to pay more for it on a standalone basis than as part of a bundle. The reality is that the broadband/TV bundle is the one most people want to buy, and AT&T has good opportunities to cross sell these two products, and that’s the most interesting part of this to me.

Hints at new products and services

One of the most intriguing things to me was several hints from executives that new products, services, or ways of delivering existing services would be coming at some point in the future. Some of the things that were hinted at included:

- Going over the top with a video service. There were several references to providing video over both managed and unmanaged networks, and the context was such that this didn’t seem to just be talking about TV Everywhere-type extensions to classic services. I’m very curious to see if this means we’re going to see either DirecTV or U-verse branded video services being sold to subscribers that can’t or don’t want to buy the traditional services from either company.

- Providing optimized video services for AT&T Mobility customers. The implication here – especially given a comment about being in compliance with merger conditions – was that AT&T might offer its mobile subscribers some special access to U-Verse or DirecTV content, or possibly use the Sponsored Data model AT&T already has in place to provide zero-rated access to this content.

- New business models for TV Everywhere authentication and sharing. There were lots of references to millennials using their parents’ pay TV login details to watch linear TV without their own subscriptions, and the opportunities to use the Mobile Share model to deal with this. That, to me, implied some sort of model under which TV subscribers would pay on some sort of per-device basis for additional streams, such that AT&T would monetize this sharing of credentials. I wouldn’t be surprised if we see more of this kind of thing from pay TV players and content owners going forward. However, TV Everywhere solutions already have a poor reputation for usability, and AT&T made portability of content a huge selling point today, so I’d expect them to tread carefully with this.

A realistic view of trends in TV

One of the things that was most refreshing about the AT&T executives’ comments during the morning was that they seem very much on top of the actual trends in the industry and not afraid of articulating them, even those that don’t necessarily bode well for traditional players. The excerpt below is from my on-the-fly notes (no transcript is available yet) based on John Stankey’s remarks on trends in the TV industry:

Pure play standalone offerings increasingly challenged. OTT will continue to grow and mature as a distribution alternative to managed networks. % of cord cutters, shavers and nevers will continue to grow. Premium content will migrate to OTT and skinny bundles. As these things occur, traditional TV advertising moves to other forms, pressuring content providers especially those with smaller audiences and less compelling content.

That seems to me both a decent summary of the trends and threats facing the traditional TV industry and a frank assessment of the implications. It’s good to see that AT&T isn’t in denial about all this (in contrast to some recent remarks from other players in the industry) and that it’s factored these trends into its projections for the combined business. In the Q&A at the end of the day, Randall Stephenson dealt with some questions on this and basically said that yes, pay TV was going to decline, but slowly, and that AT&T thought it could both grow fast enough to offset that market decline, and adapt its offerings so as to achieve similar profits off smaller TV bundles if necessary. That’s easier said than done, but given the details above about cross-selling and up-selling, it doesn’t seem too far-fetched, at least for the time being.

Two other quick notes

I don’t want to go into too much detail on this stuff, but a couple of other things were worth noting:

- AT&T’s new advertising platform and products. AT&T has now combined its old AdWorks unit with the DirecTV advertising platform, and can offer both the scale of DirecTV and the local targeting capabilities of U-verse (and will use LTE where necessary to provide targeted advertising to DirecTV subscribers). It’s interesting to see both AT&T and Verizon investing in cross-platform advertising, albeit in very different ways (Verizon through its AOL acquisition).

- John Donovan’s segment on AT&T’s technology platforms. John Donovan has been one of the best additions to the AT&T executive ranks over the last few years – he’s presided over a major overhaul of AT&T’s technology operations over the last few years, and that transformation is still going. During the conference, he talked through how AT&T is trying to match and then compound the benefits of Moore’s Law as it seeks cost efficiencies in network performance – it’s well worth a watch.

The new AT&T’s prospects

There’s so much more to talk about, and I haven’t even touched on AT&T’s Latin American strategy. But I just wanted to take a step back and summarize my view on AT&T as a company. I’ve said previously that when it comes to the mobile business, AT&T is the company most focused on what’s next. It began investing in connected cars, home automation, and a variety of other businesses years ago and is now reaping the benefits of its early start, capturing a significant share in connected cars in particular and driving significant net adds through that business. Even as the traditional phone business is saturating, AT&T is tapping into new growth areas better than its competitors, and that’s been important as its own traditional growth has slowed.

Today’s event, though, highlighted the fact that AT&T is still perfectly willing to compete in traditional areas too – the pay TV business in the US, and traditional phone services in high-growth markets like Mexico. Of course, that means exposing itself to some of those negative trends in TV, and Mexico is arguably just a few years behind the US and will eventually hit the same sort of saturation that the US has. However, in the US, its focus in the consumer market is going to be about putting together the different components of its offering in new and different ways. I expressed skepticism above about double play wireless-TV bundles, but I’m much more bullish about AT&T expanding its share of broadband-TV bundles in the AT&T footprint, especially as that footprint expands. At the same time, AT&T’s evolving technology foundation should give it the infrastructure it needs to pursue these opportunities with increasing cost efficiencies, while improving the end user experience. And on the business side, it’s continuing to build what’s arguably the strongest set of global assets for pursuing enterprise customers.

That’s a heck of a lot of moving parts, and there’s plenty of places for things to go wrong, but I’d argue that AT&T is easily the best positioned of the US carriers given its combination of assets and its strategy, and if it can execute well it should have a really good few years ahead of it.