I do a piece most quarters after the major cable, satellite, and telecoms operators have reported their TV subscriber numbers, providing an update on what is at this point a very clear cord-cutting trend. Here is this quarter’s update.

As a brief reminder, the correct way to look at cord cutting is to focus on three things:

- Year on year subscriber growth, to eliminate the cyclical factors in the market

- A totality of providers of different kinds – i.e. cable, satellite, and telco – not any one or two groups

- A totality of providers of different sizes, because smaller providers are doing worse than larger ones.

Here, then, on that basis, are this quarter’s numbers. First, here’s the view of year on year pay TV subscriber changes – a reported – for the seventeen players I track:

As you can see, there’s a very clear trend here – with one exception in Q4 2015, each quarter’s year on year decline has been worse than the previous one since Q2 2014. That’s over two years now of worsening declines. As I’ve done in previous quarters, I’m also providing a view below of what the trend looks like if you extract my estimate for DISH’s Sling subscribers, which are not classic pay TV subs but are included in its pay TV subscriber reporting:

On that basis, the trend is that much worse – hitting around 1.5 million lost subscribers year on year in Q3 2016.

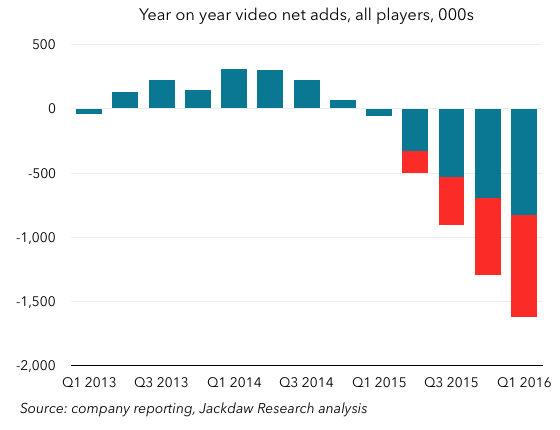

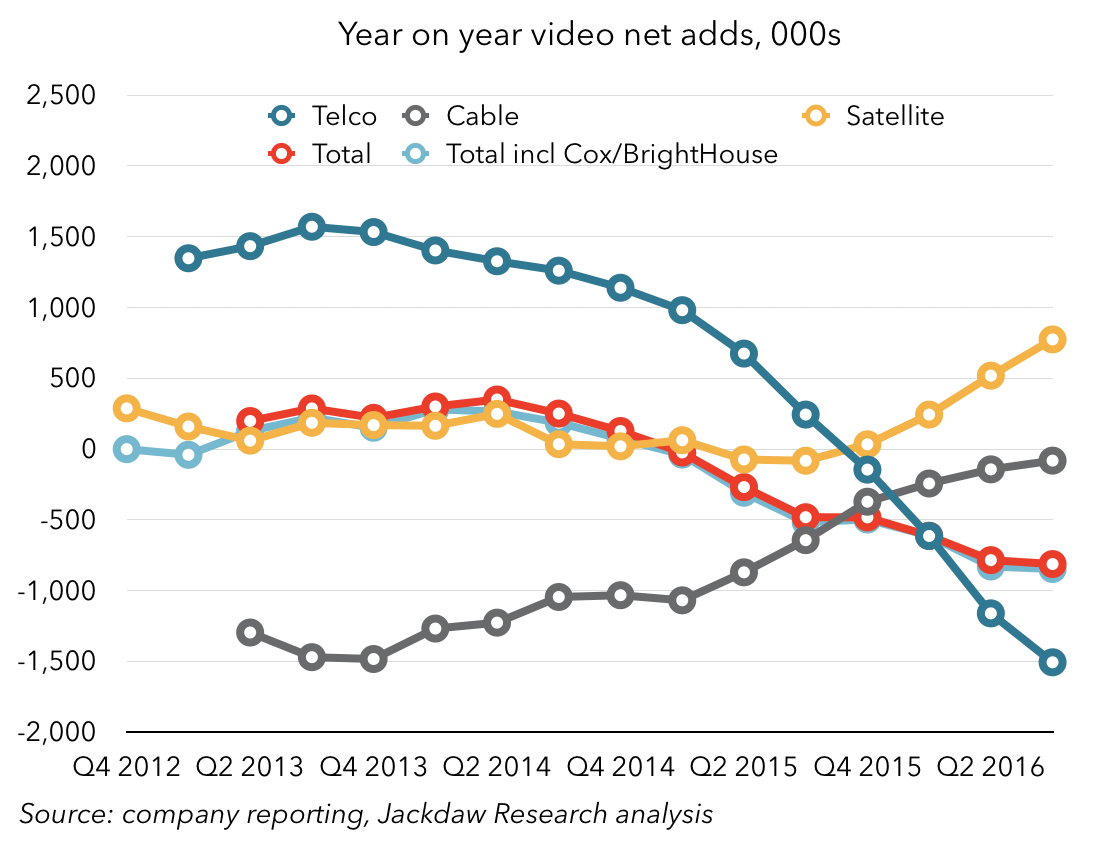

It’s also worth noting that once again these trends differ greatly by type and size of player. The chart below shows net adds by player type:

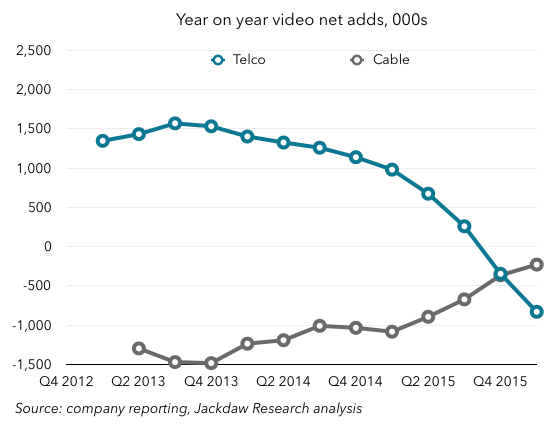

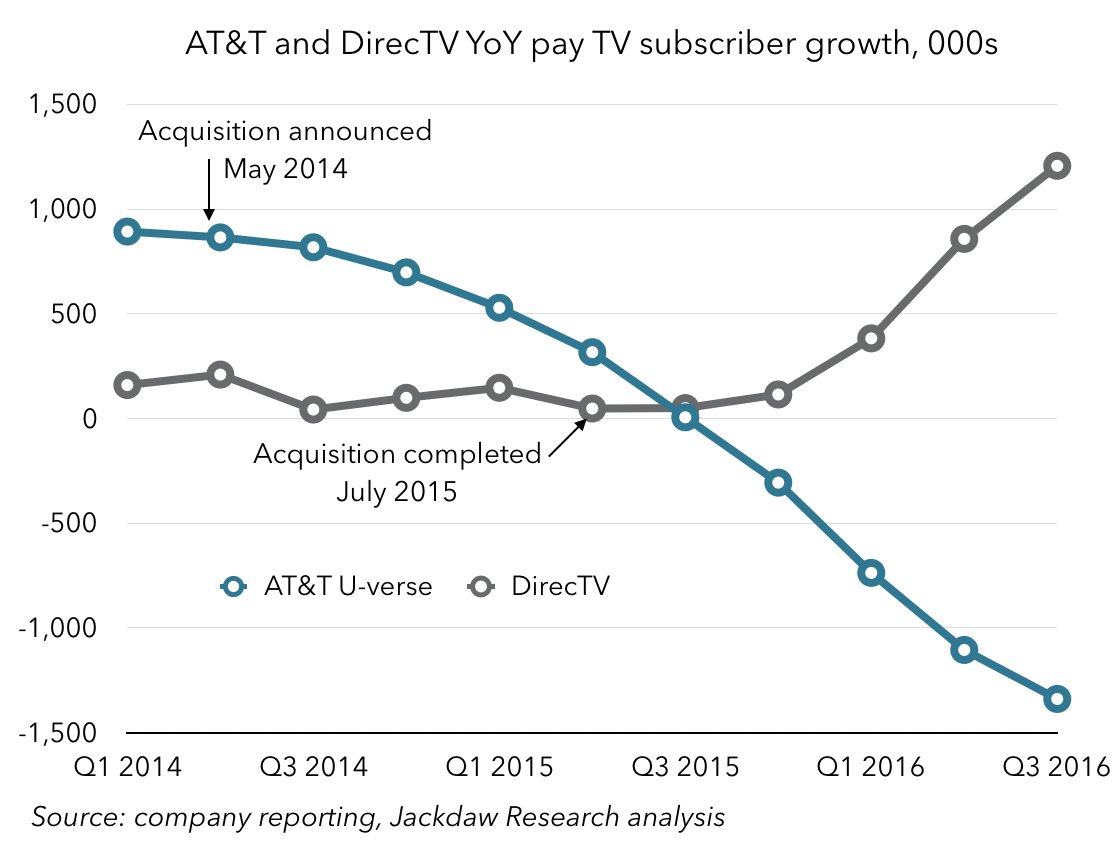

The trend here has been apparent for some time – telco subs have taken a complete nosedive since Verizon ceased expanding Fios meaningfully and since AT&T shifted all its focus to DirecTV following the announcement of the merger. Indeed, that shift in focus is extremely transparent when you look at U-verse and DirecTV subs separately:

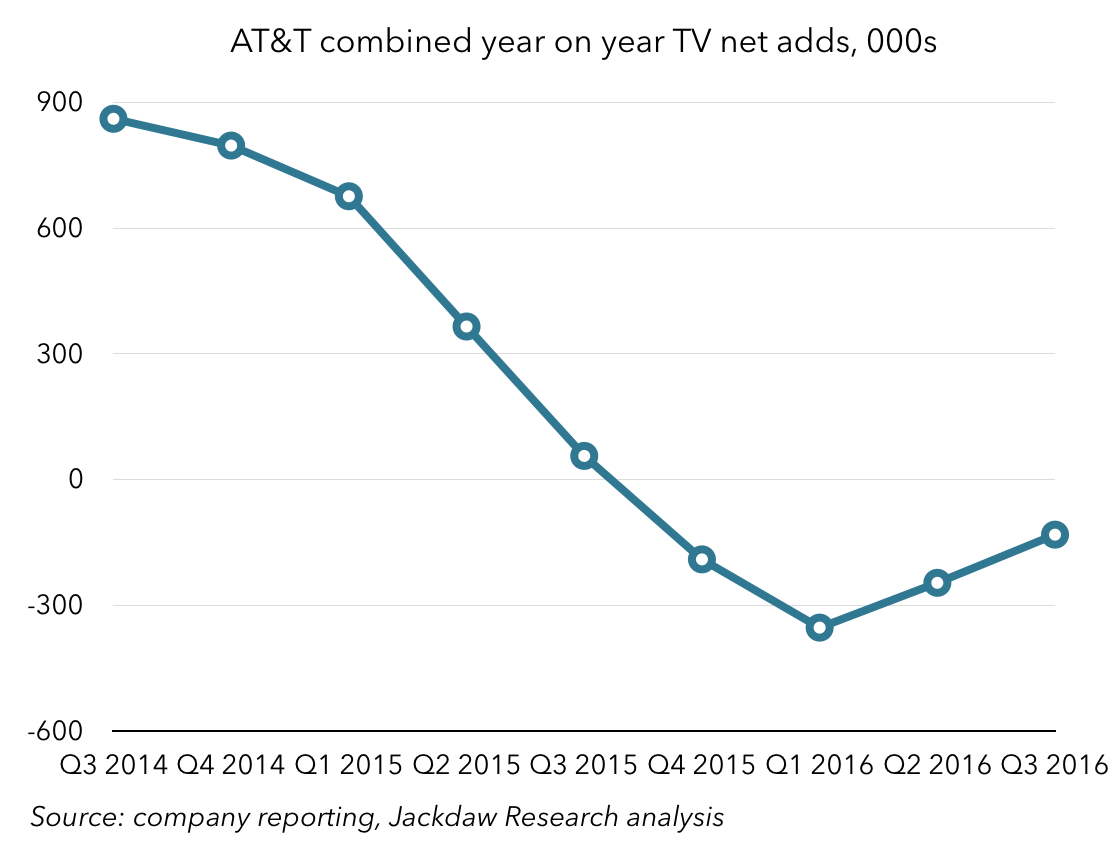

The two combined are still negative year on year, but turned a corner three quarters ago and are steadily approaching year on year parity, though not yet growth:

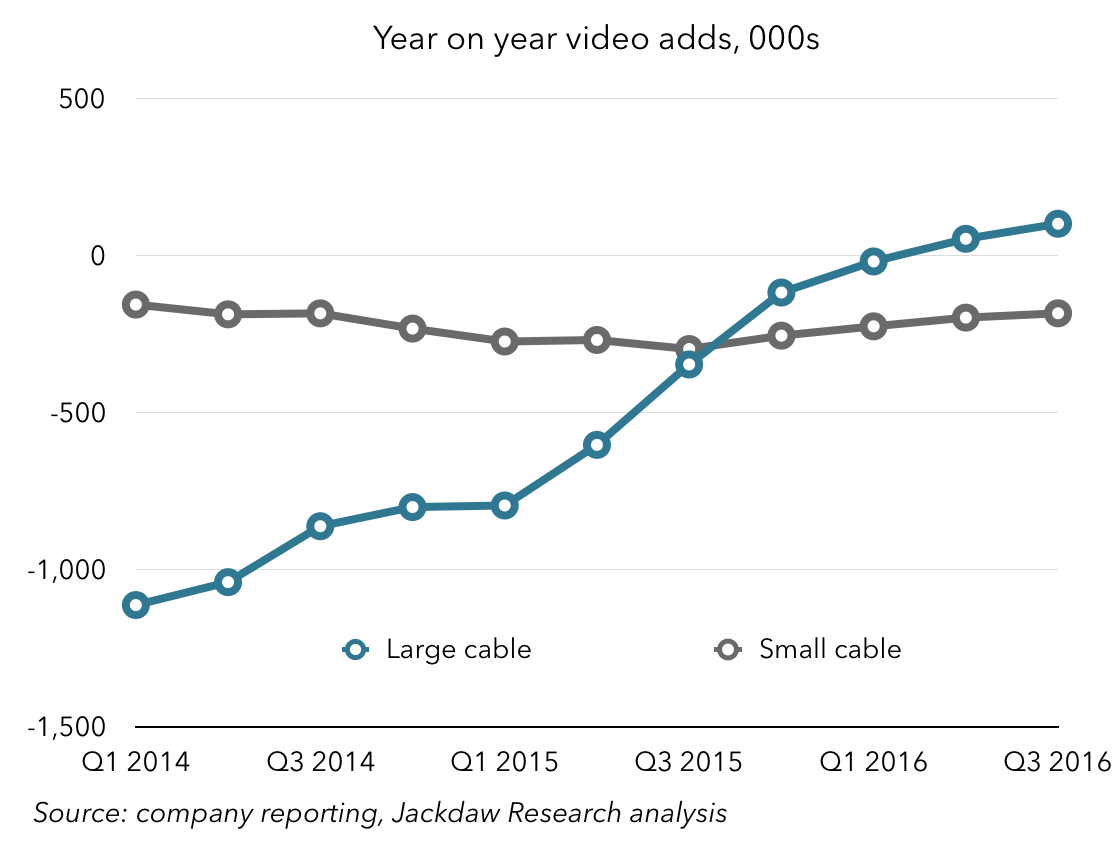

Cable, on the other hand, has been recovering somewhat, likely benefiting from the reduced focus by Verizon and AT&T on the space with their telco offerings. The cable operators I track collectively lost only 81k subscribers year on year, compared with well over a million subscribers annually throughout 2013 and 2014. Once again, that cable line masks differences between the larger and smaller operators, which saw distinct trends:

Cable, on the other hand, has been recovering somewhat, likely benefiting from the reduced focus by Verizon and AT&T on the space with their telco offerings. The cable operators I track collectively lost only 81k subscribers year on year, compared with well over a million subscribers annually throughout 2013 and 2014. Once again, that cable line masks differences between the larger and smaller operators, which saw distinct trends:

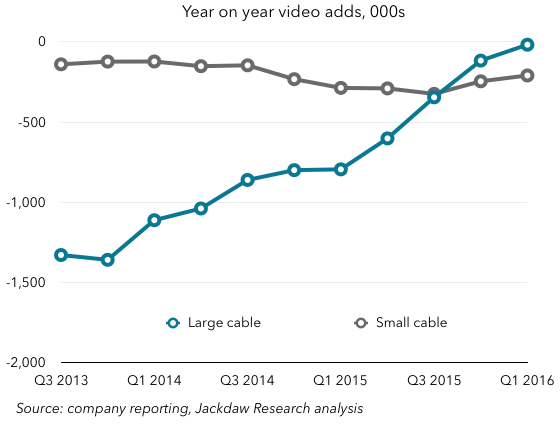

The larger cable operators have been faring better, with positive net adds collectively for the last two quarters, while smaller cable operators like Cable ONE, Mediacom, Suddenlink, and WideOpenWest collectively saw declines, which have been fairly consistent for some time now.

The improvement in the satellite line, meanwhile, is entirely due to the much healthier net adds at DirecTV, offset somewhat by DISH’s accelerating declines. Those declines would, of course, be significantly worse if we again stripped out Sling subscriber growth, which is likely at at around 600-700k annually, compared with a loss of a little over 400k subs reported by DISH in total.

A quick word on Nielsen and ESPN

Before I close, just a quick word on the Nielsen-ESPN situation that’s emerged in the last few weeks. Nielsen reported an unusually dramatic drop in subscribers for ESPN in the month of October, ESPN pushed back, Nielsen temporarily pulled the numbers while it completed a double check of the figures, and then announced it was standing by them. The total subscriber loss at ESPN was 621,000, and although this was the one that got all the attention, other major networks like CNN and Fox News lost almost as many.

In the context of the analysis above, 500-600k subs gone in a single month seems vastly disproportionate to the overall trend, which is at around 1-1.5 million per year depending on how you break down the numbers. Additionally, Q4 is traditionally one of the stronger quarters – the players I track combined actually had positive net adds in the last three fourth quarters, and I suspect for every fourth quarter before that too. That’s what makes this loss so unexpected, and why the various networks have pushed back.

However, cord cutting isn’t the only driver of subscriber losses – cord shaving is the other major driver, and that makes for a more feasible explanation here. Several major TV providers now have skinny bundles or basic packages which exclude one or more of the major networks that saw big losses. So some of the losses could have come from subscribers moving to these bundles, or switching from a big traditional package at one operator to a skinnier one elsewhere.

And of course the third possible explanation is a shift from traditional pay TV to one of the new online providers like Sling TV or Sony Vue. Nielsen’s numbers don’t capture these subscribers, and so a bigger than usual shift in that direction would cause a loss in subs for those networks even if they were part of the new packages the subscribers moved to on the digital side. The reality, of course, is that many of these digital packages are also considerably skinnier than those offered by the old school pay TV providers – DirecTV Now, which is due to launch shortly, has 100 channels, compared with 145+ on DirecTV’s base satellite package, for example.

This is the new reality for TV networks – a combination of cord cutting at 1.5 million subscribers per year combined with cord shaving that will eliminate some of their networks from some subscribers’ packages are going to lead to a massive decline in subscribership over the coming years. Significant and accelerating declines in subscribers are also in store for the pay TV providers, unless they participate in the digital alternatives as both DISH and AT&T/DirecTV are already.