Note: this blog is published by Jan Dawson, Founder and Chief Analyst at Jackdaw Research. Jackdaw Research provides research, analysis, and consulting on the consumer technology market, and works with some of the largest consumer technology companies in the world. We offer data sets on the US wireless and pay TV markets, analysis of major players in the industry, and custom consulting work ranging from hour-long phone calls to weeks-long projects. For more on Jackdaw Research and its services, please visit our website.

Microsoft reported earnings yesterday, and the highlights were all about the cloud business (Alex Wilhelm has a good summary of some of the key numbers there in this post on Mattermark). Given that I cover the consumer business, however, I’m more focused on the parts of Microsoft that target end users, which are mostly found in its More Personal Computing segment (the one exception is Office Consumer, which sits in the Productivity & Business Processes segment).

The More Personal Computing segment is made up of:

- Windows – licensing of all versions of Windows other than Windows server

- Devices – including Surface, phones, and accessories

- Gaming – including Xbox hardware, Xbox Live services, and game revenue

- Search advertising – essentially Bing.

Microsoft doesn’t report revenues for these various components explicitly, but often provides enough data points in its various SEC filings to be able to draw reasonably good conclusions about the makeup of the business. As a starting point, Microsoft does report revenue from external customers by major product line as part of its annual 10-K filing – revenue from the major product lines in the More Personal Computing Group are shown below:

Windows declining for two reasons

It’s worth noting that it appears Windows revenue has fallen off a cliff during this period. However, a big chunk of the apparent decline is due to the deferral of Windows 10 revenue, which has to be recognized over a longer period of time than revenue from earlier versions of Windows, which carried less expectation of free future updates. At the same time, the fact that Windows 10 was a free upgrade for the first year also depressed revenues. As I’ve been saying for some time now, going forward it’s going to be much tougher for Microsoft to drive meaningful revenue from Windows in the consumer market in particular, in a world where every other vendor gives their OS away for free. That means Microsoft has to find new sources of revenue in consumer: enter hardware.

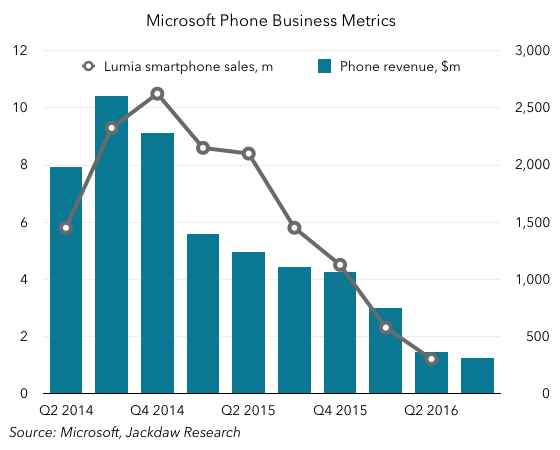

Phones – dwindling to nothing

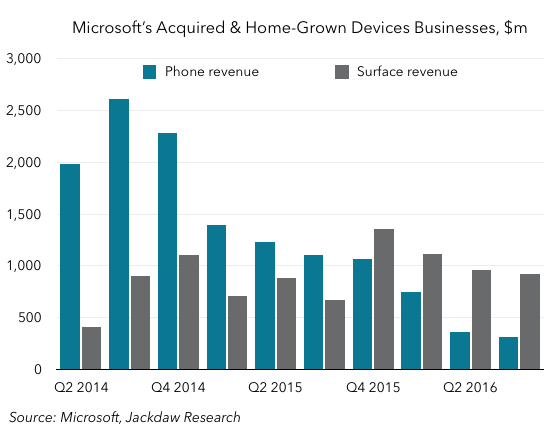

First up, phones, which appear to be rapidly dwindling to nothing. It’s become harder to find Lumia smartphone sales in Microsoft’s reporting recently, and this quarter (as far as I can tell) the company finally stopped reporting phone sales entirely. That makes sense, given that Lumia sales were likely under a million in the quarter and Microsoft is about to offload the feature phone business. The chart below shows Lumia sales up to the previous quarter, and my estimate for phone revenues for the past two years, which hit around $300 million this quarter:

Surface grows year on year but heading for a dip

Surface has been one of the bright spots of Microsoft’s hardware business over the last two years. Indeed – this home-grown hardware line has compared very favorably to that acquired phones business we were just discussing:

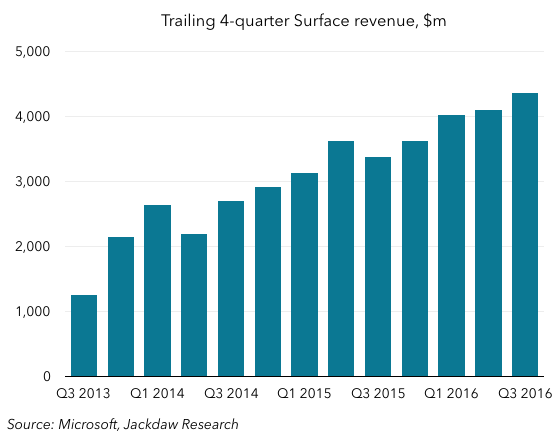

As you can see, Surface has now outsold phones for four straight quarters, and that’s not going to change any time soon. Overall, Surface revenues are growing year on year, which is easier to see if you annualize them:

However, what you can also see from that first Surface chart is that revenues for this product line are starting to settle into a pattern: big Q4 sales, followed by a steady decline through the next three quarters. That’s fine as long as there is new hardware each year to restart the cycle, but from all the reporting I’ve seen it seems the Surface Pro and Surface Book will get only spec bumps and very minor cosmetic changes, which leaves open the possibility of a year on year decline. Indeed, this is exactly what Microsoft’s guidance says will happen:

We expect surface revenue to decline as we anniversary the product launch from a year ago.

I suspect the minor refresh on the existing hardware combined with the push into a new, somewhat marginal, product category (all-in-ones) won’t be enough to drive growth. The question is whether the revenue line recovers in the New Year or whether we’ll see a whole year of declines here – that, in turn, would depress overall hardware sales already shrinking from the phone collapse.

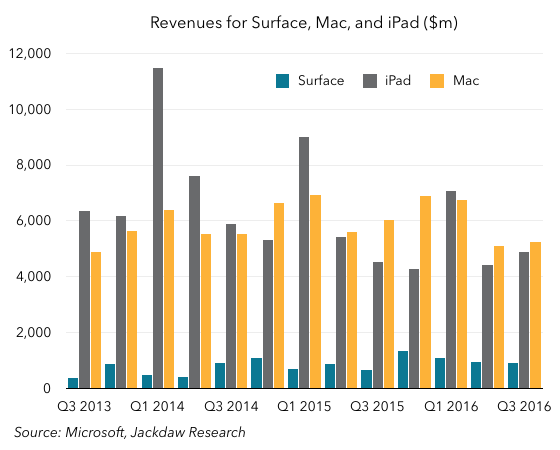

It’s also interesting to put Surface revenues in context – they’ve grown very strongly and are now a useful contributor to Microsoft’s overall business, but they pale in comparison to both iPad and Mac sales, neither of which have been growing much recently:

Ahead of next week’s Microsoft and Apple events, that context is worth remembering – for all the fanfare around Surface, Microsoft’s computing hardware business is still a fraction of the size of Apple’s.

Gaming – an oldie but kind of a goodie

Gaming, of course, is the oldest of Microsoft’s consumer hardware businesses, but its gaming revenue is actually about more than just selling consoles – it also includes Xbox Live service revenues and revenues from selling its own games (now including Minecraft) and royalties from third party games. However, it’s likely that console sales still dominate this segment. Below is my estimate for Gaming revenue:

In fact, Microsoft actually began reporting this revenue line this quarter, though unaccountably only for this quarter, and not for past quarters. Still, it’s obvious from my estimates that this, too, is an enormously cyclical business, with a big spike in Q4 driven by console sales and to a lesser extent game purchases, followed by a much smaller revenue number in Q1 and a steady build through Q3 before repeating. Microsoft no longer reports console sales either, sadly, likely because it was coming second to Sony much of the time before it stopped reporting. Still, gaming makes up almost a third of MPC segment revenues in Q4, and anything from 8-20% of the total in other quarters. In total, hardware likely now accounts for 30-50% of total revenue from the segment quarterly.

Search advertising – Microsoft’s quiet success story

With all the attention on cloud, and the hardware and Windows businesses going through a bit of a tough patch, it’d be easy to assume there were no other bright spots. And yet search advertising continues to be the undersold success story at Microsoft over the last couple of years. I’ve previously pointed out the very different trajectories of the display and search ad businesses at Microsoft, which ultimately resulted in the separation of the display business, but the upward trajectory of search advertising has accelerated since that decision was made.

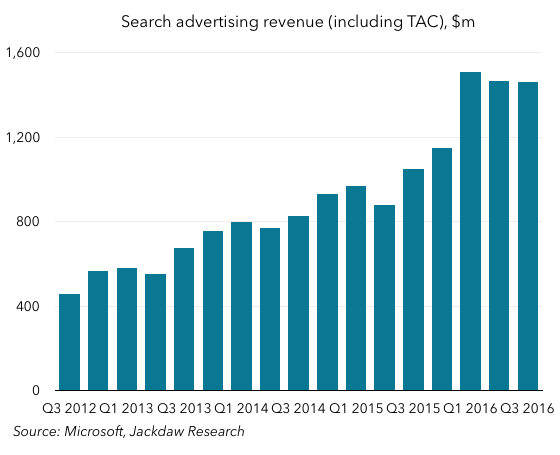

Again, Microsoft doesn’t report this revenue line directly, but we can do a decent job of estimating it, as shown in the chart below:

There are actually two different revenue lines associated with search advertising – what I’ve shown here is total actual revenue including traffic acquisition costs, but Microsoft tends to focus at least some of its commentary on earnings calls on a different number – search revenue ex-TAC. As you can see, the total number has plateaued over the last three quarters according to my estimates, though the year on year growth numbers are still strong. However, the ex-TAC number is growing more slowly. In other words, this growth is coming at the expense of higher traffic acquisition costs, which seems to be the result of the deal Microsoft signed with Yahoo a few quarters ago and an associated change in revenue recognition. Still, it’s a useful business now in its own right, with advertising generating 7% of Microsoft’s revenues in the most recent fiscal year.